Ancova Energy Market Update

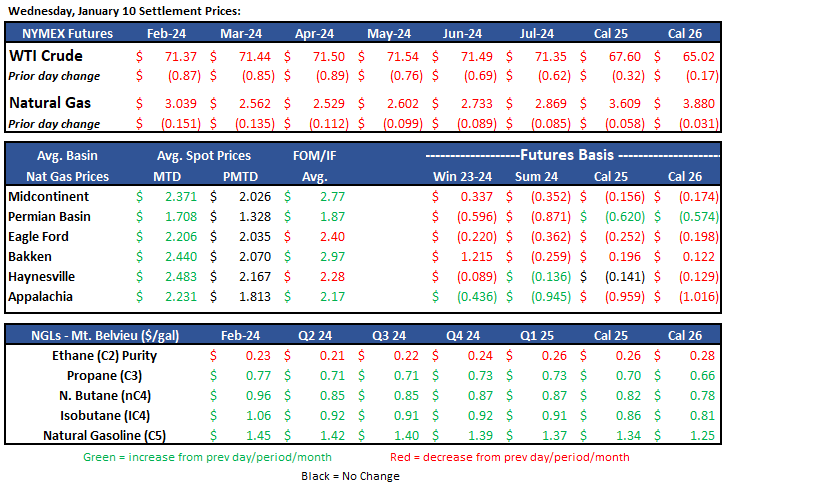

Current Market Pricing

Crude Oil

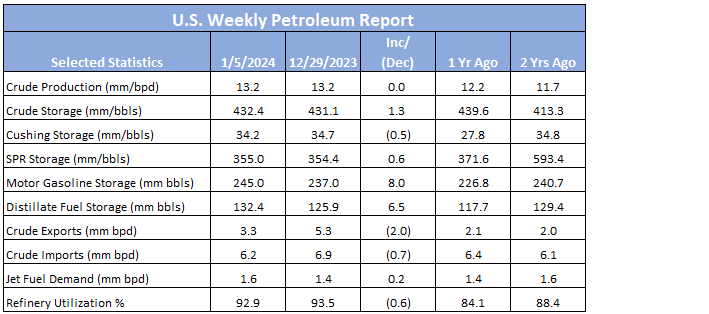

Prompt-month WTI traded $0.87 lower yesterday, closing the session at $71.37/bbl. The contract has reversed majority of that loss today, slightly above $72 in early afternoon trading on news that Iran seized an oil tanker in the Gulf of Oman, further destabilizing an already unstable situation in the region. U.S. crude storage added ~1.3mm bbl, according to the EIA, but the Cushing hub saw a 0.5mm bbl decline from the previous week. Worth noting that crude inventories are still 9-10mm bbls below the 5yr avg., keeping a floor on WTI. Other petroleum products, namely motor gasoline and distillates (diesel, jet fuel, kerosene) saw significant inventory builds at 8mm and 6.5mm bbls, respectively, which is not unusual for this time of year. With production remaining high and demand continuing to slow, near term pricing in the $70s seems to be the logical range.

Full Report here: U.S. Weekly Petroleum Report

Rig Count

The U.S. oil and gas rig count edged up two on the week to 677, which is still hovering around a two-year low. SCOOP+STACK combined play added roughly 10% or three rigs on the week despite dropping 17 over the course of a year. Haynesville added the biggest gain by the numbers, increasing four to 58 active.

Natural Gas

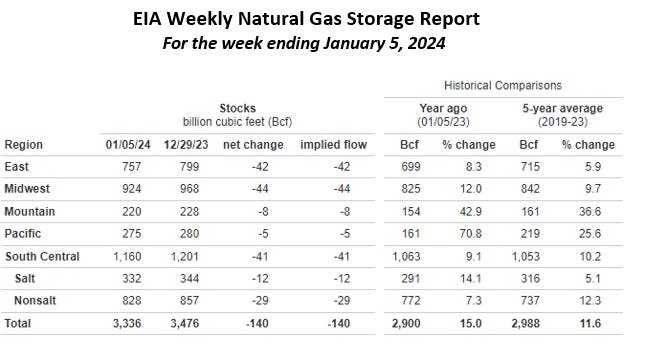

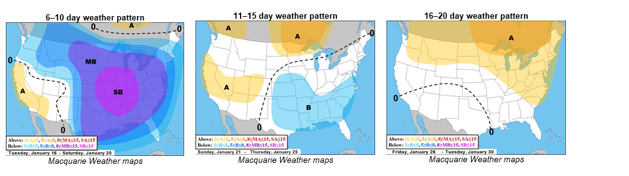

With the much-anticipated artic weather in the forecast, natural gas futures made their way above the $3.00 mark to kick off the week. While the market saw six straight sessions of gain, prices have managed to stay at or around the $3 mark for most of the week. Below zero wind chills are predicted early next week with a deep freeze forecasted as far south as central Texas. Demand looks to surge this weekend and into early next week as the cold wave sweeps across the U.S. Eyes will be on Texas with the state issued warnings of potential stress on the power grids due to extreme cold temps. A 140 Bcf withdrawal reported by the EIA this morning has the market with bulls, but a late January warm-up could bring back the bears.

With a 3% increase of inflows into the Midcontinent, prices for next day flows mostly fell. This morning’s spot prices has Chicago city-gates trading a $.33 discount to Henry Hub at $2.90 while ANR is $.40 back and NGPL is sitting $.43 back. In the futures market, Chicago city-gates is trading a $1.16 premium to Henry Hub while ANR OK and NGPL are both premiums at $1.38 and $.56 respectively. According to S&P Global Commodity Insights data, Midcontinent demand is expecting an increase to 27.53 Bcf/d as temperatures in the Midcon market area are forecasted to be well below average this weekend.

The EIA released storage numbers this morning, coming in at 3,336 Bcf, representing a net -140 Bcf decrease from the previous week. This decrease was above the marketplace withdrawal expectations range of -105 to -122 Bcf. Stocks were 436 Bcf less this time last year, however, this week’s levels are still within the 5 yr. historical range of 2,988 Bcf.

Natural Gas Liquids

Some big % movements in product prices across both Mont Belvieu and Conway, with ethane leading the way at 24% and 31%, respectively. With winter showing up across several key market areas, propane saw a strong bump from same period a week ago, adding 15% and 19%, respectively. All other products kept in a fairly tight pricing range (+/- 5%) compared to last week.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.