Ancova Energy Market Update

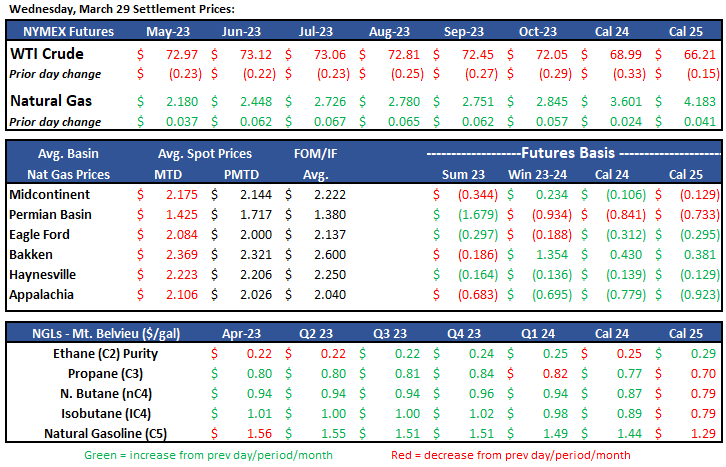

Market Pricing

Crude Oil

The prompt month crude contract has been steadily increasing over the last few weeks, despite settling $0.23/bbl lower yesterday at $72.97. Early afternoon trading today has the contract up $1.39 to $74.36, driven by a weak U.S. dollar and a 7.5mm bbl decline in crude inventories (5.9mm bbl expectation), which is at a 6-week low. Strong Chinese refinery run rates are also indicating that the country’s demand is coming back full force. Other bullish factors include elevated global air traffic, and U.S. diesel and gasoline storage levels significantly below 5-year averages. However, on the bear side, additional rate hikes by the Fed are likely, which could slow down the economy.

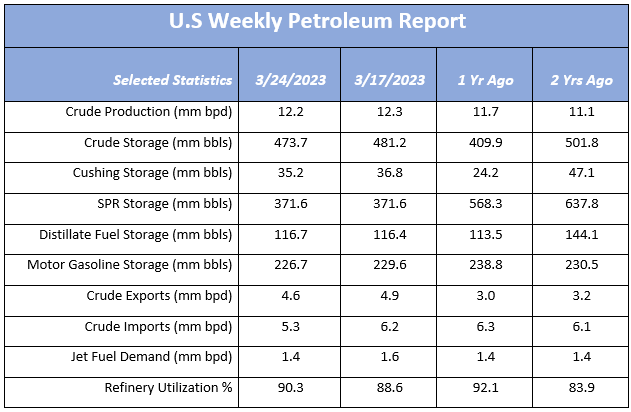

The EIA released its weekly report yesterday. Cushing storage drops again by 1.6mm bbls, which is about 11mm bbls higher than same period last year. Refinery run rates continue to increase, with the last data showing a 1.7% increase and now over 90% on average across the U.S. Production dropped slightly to 12.2mm bpd. See additional details below and click the link for the full report.

Additional data at: www.eia.gov/petroleum/supply/weekly

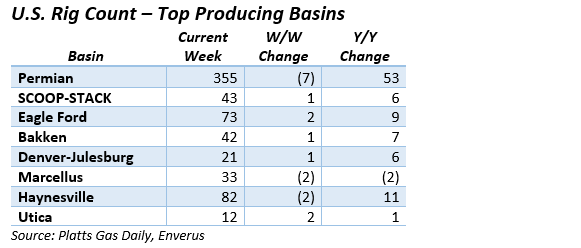

Current Rig Count

The US oil and gas rig count increased by one rig last week, bringing the total active rigs to 839. The Permian basin, the largest oil-producing basin in the country, saw the biggest drop with a loss of seven rigs. Despite this, the basin still has 53 more active rigs than it did a year ago. On the other hand, the remaining oil plays added a combined five rigs, while the gas-heavy basins saw a net two-rig decrease. As a result, there are now 638 oil rigs and 201 natural gas rigs.

Natural Gas

With forecasts pointing toward mild springtime demand, Natural Gas futures continued to be lack-luster this week. After opening at $2.13 to start the week, prices had fallen below $2.00 by mid-week. The below $2 mark should propel a switch from coal to gas in some areas and could provide a much-needed positive in the long term. Freeport’s LNG facility looks to be in full operation and on track to reach 2.1 Bcf/d as early as today. Freeport is responsible for 20% of the total US LNG exports and their return to full capacity is important for Europe’s LNG concerns. Even though the mild winter weather and lower consumption has helped Europe manage their gas supply, additional LNG exports could go far in easing concerns. With storage over 20% above the 5 yr. avg, the market looks to stay with the bears.

With demand expected to drop across the region, Midcon cash prices dipped as well. Chicago city-gates was down to $2/MMBtu with Oneok tumbling to $1.75/MMBtu and NGPL to $1.85/MMBtu. In the forwards market, Chicago CG comes in $.02 over Henry Hub while ANR OK and NGPL Midcon are -$.07 and -$.19 back respectively. Total demand in the Midcon is down to 20.3 Bcf/d, a decrease of 2.8 Bcf/d with residential demand accounting for 2.5 Bcf/d of the drop. Net flows into the Midcon saw a 10% increase over this same time last year, coming in at 9.6 Bcf/d according to S&P Global Commodity Insights.

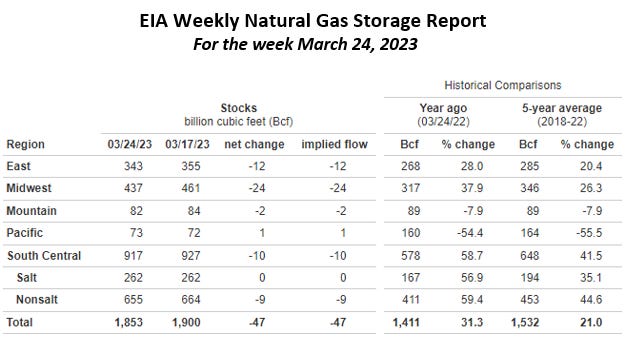

The EIA released storage numbers this morning, coming in at 1,853 Bcf, representing a net -47 Bcf decrease from the previous week. This decrease was slightly less than marketplace expectations of –52 Bcf decrease. Stocks were 442 Bcf less this time last year and come in 321 Bcf above the 5 yr. historical range of 1,532 Bcf.

Natural Gas Liquids (NGLs)

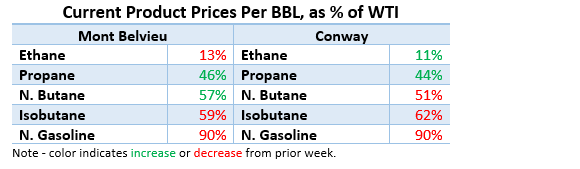

In Mont Belvieu, prompt-month product prices were mixed, with Propane, N. Butane, and N. Gasolines all higher, while purity Ethane and Isobutane were lower. In contrast, all Conway products were higher, with Ethane and Propane leading the pack. Isobutane was the only loser, falling 3% from the same period a week ago.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.