Ancova Energy Market Update

Select Market Pricing

Crude Oil

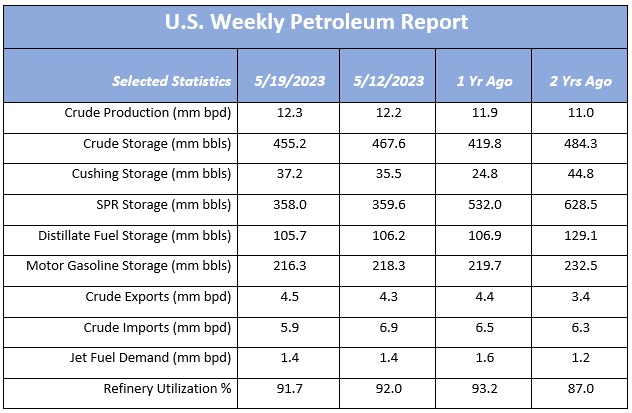

The June 2023 contract faded into the books just under $72 at 71.99/bbl. July, the new prompt month contract closed yesterday $1.43 higher to $74.34 before moving sharply the other direction - down $2.66 in early afternoon trading to $71.68/bbl. Yesterday’s positive movement was on the heels of the large crude draw reported by the EIA (12.4mm bbls) but today’s downward shift might indicate poor debt ceiling negotiations along with additional possible interest rate hikes here in the U.S and abroad. As rig counts continue to drop (see below), it’s only a matter of time before it shows up on the production/supply side which is what many analysts are making their $80-$90/bbl crude bets by year-end on.

www.eia.gov/petroleum/supply/weekly

Rig Count Update

The U.S. rig count continues to drop, down six from prior week to 783. Total rigs sat at 864 late January. The Permian rig count has held up throughout the year, only down three rigs at 354. The Haynesville and Eagle Ford have accounted for roughly half of the rig drops at 20 and 19, respectively.

Natural Gas

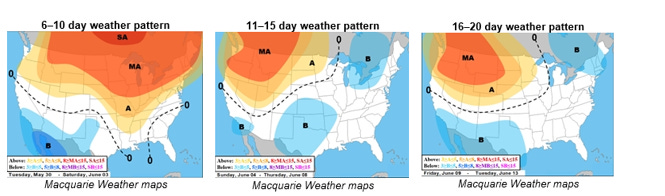

After last week’s strong rally, Nat Gas prices have trickled downward this week, erasing much of the gain. Monday’s opening of $2.58 has been the high mark for the week as a slightly cooler weather forecast has contributed to quieting the rally. The extended forecast does look to bring in warmer temps as we head into June, which should provide a jump in power burn demand. The US rig count looks to continue the downward trend and LNG floating storage is down from last week, both making a case for trimming the oversupplied market. For now, all eyes will be on the weather forecast as a warmer than normal summer season will be needed to pry the market from the bears.

Demand is starting to rise in the Midcon, however, Chicago city-gates fell to $2.05/MMBtu, with Oneok and NGPL coming in at $2.05 and $2.04 respectively. In the futures market, Chicago city-gates is $.20 back from Henry Hub, while ANR OK and NGPL Midcon are $.24 and $.26 back. Total demand in the Midcon was projected to grow to 14.16 Bcf/d, an increase of 717 MMcf/d. With Tennessee Gas Pipeline switching flow direction and now sending gas into the Lower Midcontinent, eyes are on an already high Midcontinent regional storage that is 1.6 Bcf/d above last year’s summer levels, according to S&P Global data.

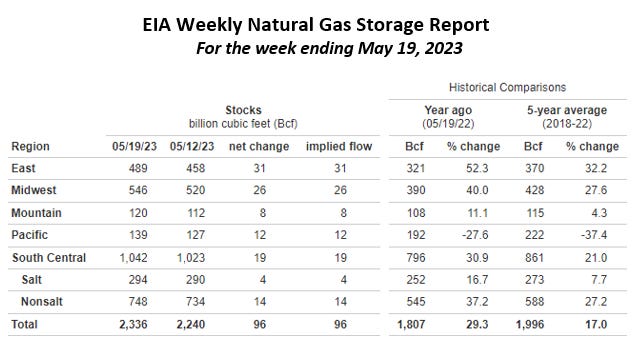

The EIA released storage numbers this morning, coming in at 2,336 Bcf, representing a net +96 Bcf increase from the previous week. This increase was slightly less than marketplace expectations of +97 Bcf increase. Stocks were 529 Bcf less this time last year and come in 340 Bcf above the 5 yr. historical range of 1,996 Bcf.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.