Ancova Energy Market Update

Current Market Pricing

Crude Oil

The prompt-month contract added $2.32 in yesterday’s session, closing at $72.70/bbl on news that Libya’s largest oil field (+ 300k bopd) has been shut in with no clear timing on returning to production. The API released its weekly U.S. storage report yesterday, indicating a huge 7.4mm bbl draw, also helped push crude prices higher. The much more reliable EIA report was released this morning (delayed a day due to Monday being a holiday) showing a significant but less dramatic draw of 5.5mm bbls against a 2-3mm bbl expectation. Despite the recent bullish drivers a prompt-month price in the low $70 range appears to be the sweet spot given the seasonal slow in demand coupled with record U.S. production. The contract is slightly lower as the current day session comes to a close, currently $0.32 lower at $72.38/bbl.

Full report here: U.S. Weekly Petroleum Report

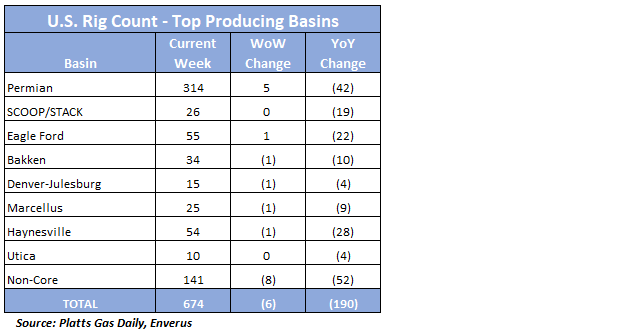

U.S. Rig Count

The U.S. oil and natural gas rig count dropped six on the week ending Dec 20th to 674, hitting a 25-month low. With the exception of the Permian (+5), there was little movement across the major basins as non-core areas combined for an eight rig drop. The overall rig count is off by nearly 200 YoY as commodity prices have softened throughout 2023.

Natural Gas

As post-holiday weather continues the cooler pattern, natural gas futures have reaped the benefits. After an opening of $2.60 to start the new year, prices have been steady this week and were trading near the $2.90 range this morning. US heating demand looks to get a kick start as the longer-range forecast is calling for a Canadian air mass to cover the upper Midwest. With much of the winter still in front of us, a seasonal rally is not out of the picture. While US LNG exports remain at record levels, thoughts of Red Sea disruptions are adding to an unstable situation in the global LNG market and could have major impacts on LNG prices this winter. February natural gas futures look to remain in a bearish structure; however, the bulls will make a run if prices continue to push $3.00.

A colder forecast and an increase in demand has prices in the Midcontinent on the uptick. This morning’s spot prices had Chicago city-gates trading a $.13 discount to Henry Hub at $2.47 while ANR was $.14 back and NGPL sat $.25 back. In the futures market, Chicago city-gates was trading a $.45 premium to Henry Hub while ANR OK and NGPL were both premiums at $.38 and $.12 respectively. According to S&P Global Commodity Insights data, Midcontinent demand is expecting an increase of over a 1 Bcf/d as temperatures in the Midcon market area are forecasted to be below average for the first two weeks of 2024.

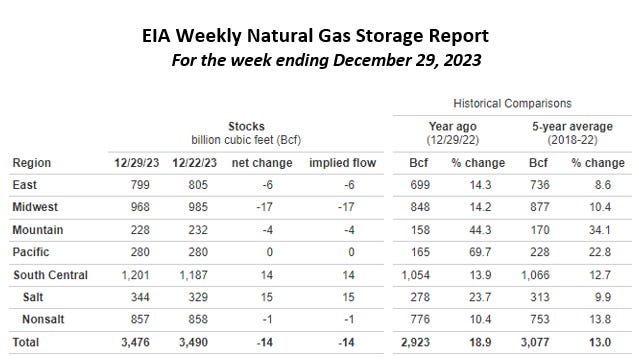

The EIA released storage numbers this morning, coming in at 3,476 Bcf, representing a net -14 Bcf decrease from the previous week. This decrease was below the marketplace withdrawal expectations range of -20 to -55 Bcf. Stocks were 553 Bcf less this time last year, however, this week’s levels are still within the 5 yr. historical range of 3,077 Bcf.

Natural Gas Liquids

Products in both Mont Belvieu and Conway were mixed compared to week ago prices - MB Ethane was ~2c or 9% higher, Conway Isobutane was 10c or 7% higher, and Conway Propane was 3.5c or 5% higher. MB N. Butane and Conway N. Gasoline were both 4% while Conway Ethane was flat on the week.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.