Ancova Energy Market Update

Select Market Pricing

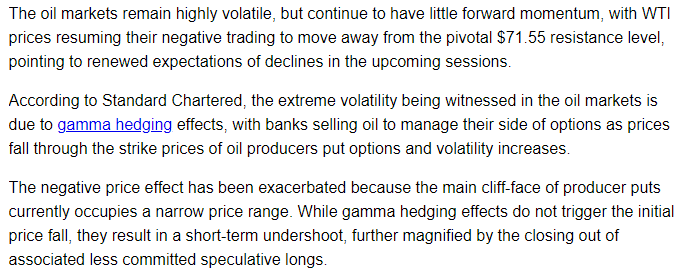

Crude Oil

The prompt month contract bounced around in a somewhat tight range week on week, closing $1.97 higher to $72.83 yesterday despite the EIA news of a 5mm bbl storage build which included a 1.5mm bbl build at Cushing. The contract settled at $72.56 same period a week ago, dipping into the $60s for short stints but never closing below $70/bbl. Gasoline and diesel inventories continue to draw down and remain below their 5yr averages, supporting both crude prices and refining margins. As we continue to move into driving/traveling season, these tight gasoline and diesel markets are bullish signs, however, but many investors/speculators remain cautious, citing concerns of economic growth or even potential recession later this year, early next.

This OilPrice.com piece from Alex Kimani provides some color into non-supply/demand fundamentals creating volatility in crude prices.

Crystal clear. He goes on to quote Goldman Sachs commodity research executive Jeff Currie who recently predicted that crude prices could eclipse $100/bbl again, possibly by year end - “Are we going to run out of spare production capacity? Potentially by 2024, you start to have a serous problems.” Last month, Goldman advised investors to move heavy into energy and mining stocks, stating both sectors are positioned well to benefit from China’s economic growth. Their current forecast includes a 23% boost in WTI over the next 12 months fueled by a supply crunch from the OPEC+ cuts put in place this month.

www.eia.gov/petroleum/supply/weekly

Rig Count Update

The overall U.S. rig count dropped 13 rigs from previous week to 790, which makes it the lowest average weekly amount in over a year. The losses were basically split, with oil rigs losing six (621 active) with gas rigs losing seven (169 active). The Bakken saw the biggest movement in both count and percentage while shedding five rigs (~12%). The most active gas play, the Haynesville, dropped three down to 64 and is now 16 rigs lower from a year ago.

Natural Gas

Several noteworthy items have contributed to the $.10-$.15 jump in Natural Gas prices this week. Canadian wildfires, power generation records and a declining rig count has the market doing its bullish impersonation. As fires sweep across the western part of Canada, the oil and gas industry is feeling the impact. With many of the major drillers having already shut in production, a large part of Canada’s Alberta shale producing regions remain under extreme wildfire warnings. Natural gas consumption for power generation is forecasted to reach the highest on record this summer, according to Energy Information Administration (“EIA”) and the lower gas prices have finally grabbed producer’s attention as the rig count continues to drop. The positive movement this week has cast hope with traders but time will tell if the market can sway away from the bears.

With the demand continuing to weaken in the Midcon, spot prices fell across the board. Chicago city-gates fell to $2.16/MMBtu, while Oneok and NGPL came in at $2.15 and $2.05 respectively. In the futures market, Chicago city-gates is $.13 back from Henry Hub, while ANR OK and NGPL Midcon are $.23 and $.25 back. Total demand in the Midcon was projected to drop to 14.29 Bcf/d, a decrease of 758 MMcf/d. In the Midcon producing region, power demand was expected to decrease to 1.44 Bcf/d, with res-comm demand forecasted to decrease 62 MMcf/d to 1.44 Bcf/d. According to S&P Global, supply in the Midcon is 3% lower than the month-to-date supply last year.

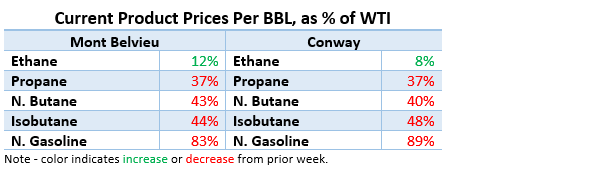

Natural Gas Liquids

Product prices in both MB and Conway were lower WoW with exception of Ethanes, which were 5% and 3% higher, respectively. Isobutanes in both markets showed the biggest decreases at 7% and 12%, respectively. Natural Gasolines were impacted the least at 3% and 1%, respectively.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.