Ancova Energy Market Update

Current Market Pricing

Crude Oil

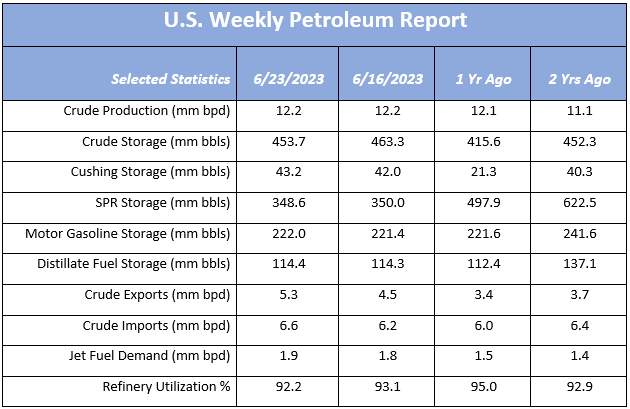

Prompt-month crude contract reversed some of its earlier losses in the week yesterday, closing $1.86 higher to $69.56/bbl. Prices are fairly flat today as the market doesn’t quite know what to do with the 9mm bbl crude inventory decline (now 6.6mm bbls below 5yr avg.) and elevated travel demand against potential rising interest rates and fears of a global recession. The OPEC folks have also made comments that they will discuss at their next meeting making the latest production cuts permanent. WTI appears to be tied in to that +/-$70 mark and it remains to be seen what’s going to get it off high center.

www.eia.gov/petroleum/supply/weekly

Rig Count

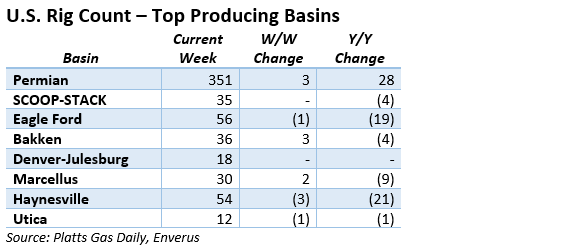

The U.S. oil and gas rig count bucked a six-week losing trend (-60) by picking up a net four rigs on the week to 747. For reference, the rig count began the year at 866 or 119 higher than the current count. Permian and Bakken both picked up three rigs while Haynesville dropped three.

Natural Gas

Natural Gas has managed to stay with the bulls this week as prices neared the $3 mark. With record-breaking demand covering the southern US, a large portion of the US is still experiencing mild temperatures. The heat has made its way north into Kansas and Missouri but how far it expands into the US seems to be the key. As the EIA reported this week, US natural gas demand has increased 43% from 2012 to 2022. While LNG exports account for a majority of the increase, a large demand driver has been the increase in natural gas-fired electric power generation. With air conditioning demand continuing to increase each of the last five years, the switch from coal-to-natural gas has led to significant demand growth. The market looks to continue riding the heat wave as the longer-term forecast shows heat build in the coming weeks.

Natural gas spot prices have been mixed in the Midcon this week, despite an increase in demand. Chicago city-gates spot prices come in a $.26 discount to Henry Hub while NGPL is $.26 back and ANR is $.30. In the futures market, Chicago city-gates is $.24 discount to Henry Hub while ANR OK and NGPL Midcon are $.29 and $.22 back. Total demand in the Midcon is forecasted to hit 14.26 Bcf/d, an increase of 141 MMcf/d. In the Midcon producing region, residential-commercial demand is expected to reach 1.91 Bcf/d with power demand reaching 2.09 Bcf/d, according to S&P Global Commodity Insights data. Additionally, Midcon production has declined to 10.23 Bcf/d, with Anadarko-KS increasing 25MMcf/d and Anadarko-OK dropping 79 MMcf/d.

The EIA released storage numbers this morning, coming in at 2,805 Bcf, representing a net +76 Bcf increase from the previous week. This increase was slightly less than marketplace expectations of +78-83 Bcf increase. Stocks were 566 Bcf less this time last year and come in 358 Bcf above the 5 yr. historical range of 2,447 Bcf.

Natural Gas Liquids

Products in both markets were down across the board, with exception of MB ethane which enjoyed a solid 18% increase from same period a week ago. Conway ethane on the other hand dropped another 13% WoW. The remaining product prices fell anywhere from 3-8%.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.