Ancova Energy Market Update

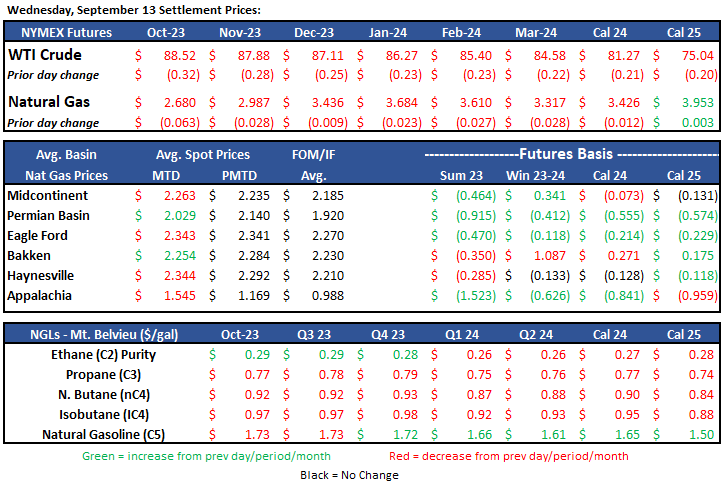

Current Market Pricing

Crude Oil

The prompt-month contract retreated slightly yesterday on the heals of a +4mm bbl storage number released by the EIA, falling $0.32 to $88.52/bbl. Yesterday’s loss was quickly reversed in today’s trading, with the Oct 2023 contract currently $1.83 higher and eclipsing the $90/bbl mark to $90.35. The positive news being the IEA (not to be confused with the EIA) making the assertion that global oil supplies could be running at a 1.2mm bpd deficit into the 4th quarter of this year, even as U.S. production continues to show strength. Global demand also remains strong for this time of year and the overall theme right now supporting higher prices is the looming supply crunch.

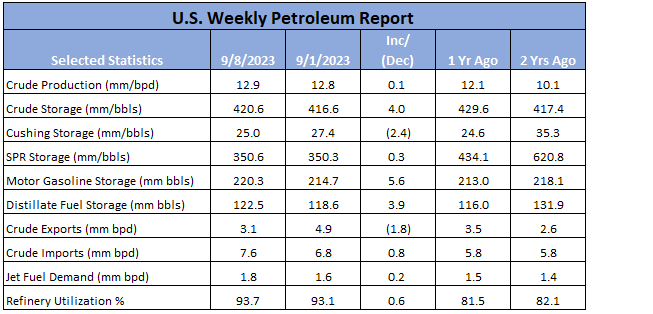

Full Report Here: U.S. Weekly Petroleum Report

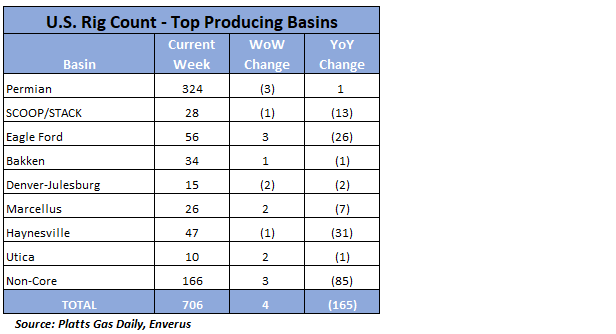

U.S Rig Count Update

The U.S. oil and gas rig count reversed course, adding four rigs on the week to 706. Oil focused rigs picked up five to 583 while the gas focused count dropped a single rig to 123. Although the overall gain was subtle, the number of private companies adding rigs has seen a significant increase - gaining 22 rigs over the last two weeks alone as oil prices have continued to climb. The year-to-year change has also been significant, yet in a different direction, losing 165 rigs (160 alone in 2023) primarily from the Eagle Ford, Haynesville, and non-core basins. Despite the drop on the week, the Permian is actually a single rig higher than the same period a year ago. Andy Hendricks, CEO of Patterson-UTI, stated in a conference on Sept 5 that he is showing a decent increase in rig totals beginning in Q4 of this year based on recently signed contracts.

Natural Gas

After opening the week at $2.61, natural gas futures rallied into the $2.80 range in early morning trading. As crude prices have cruised this week, natural gas prices have gained momentum. With prices typically in a seasonal low this time of year, demand remains elevated with tropical activity and thoughts of early cold weather entering the picture. European storage remains healthy, however, the escalation of the LNG worker’s strike in Australia and China making an appearance on the spot market to secure wintertime deliveries are adding to an already volatile LNG market. As rig counts continue to drop (53 below this time last year) and focus shifts to winter demand expectations, natural gas prices will look to stay with the bulls in the near term.

With demand in the Midcontinent seeing an increase this week, spot prices increased as well. Chicago city-gates spot prices are a $.42 discount to Henry Hub at $2.34 while ANR and NGPL are $.55 and $.48 back. In the futures market, Chicago city-gates is trading a $.39 discount to Henry Hub while ANR OK and NGPL Midcon are $.44 and $.48 back. According to S&P Global Commodity Insights data, total demand in the Midcon is expected to come in at 14.12 Bcf/d. In the Midcon producing region, power demand is just under 1.6 Bcf/d and res-comm demand is just above 2 Bcf/d. Month-to-date supply in the Midcon is sitting 3% below this same time last year with production in the area increasing by 1% and inflows decreasing by 6%.

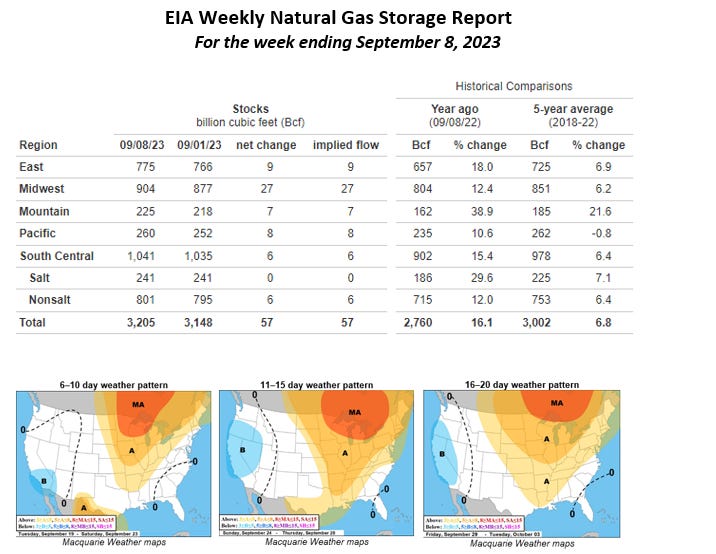

The EIA released storage numbers this morning, coming in at 3,205 Bcf, representing a net +57 Bcf increase from the previous week. Stocks were 445 Bcf less this time last year and come in 203 Bcf above the 5 yr. historical range of 3,002 Bcf.

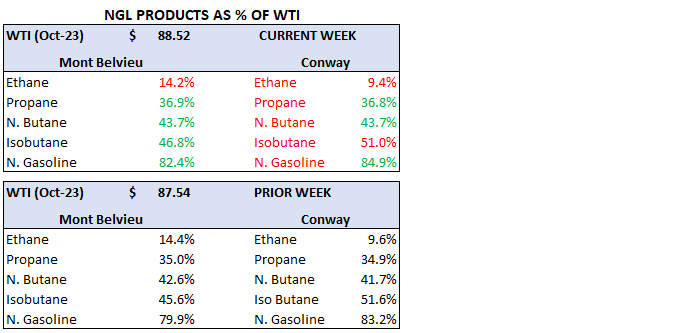

Natural Gas Liquids

Product prices in both Mont Belvieu and Conway were mostly positive week on week, with exception of Ethane in both markets (0% and -1%, respectively). All other products increase in the 3-4% range, on par with crude oil.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.