Ancova Energy Market Update

Current Market Pricing

Crude Oil

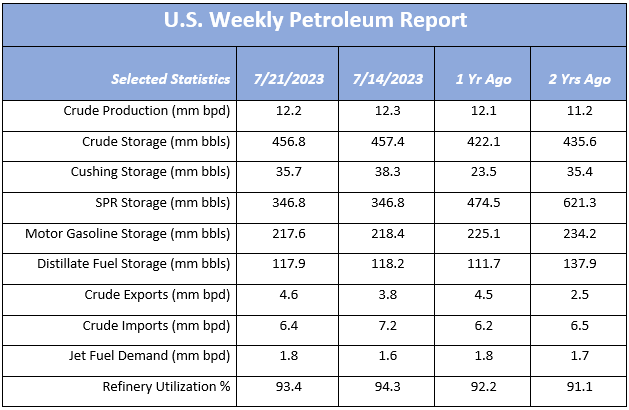

The Aug 2023 crude contract rolled off the board late last week up $0.28 to $75.63/bbl. Since the new prompt month contract (Sept 2023) rolled on, it’s been moving higher and hit north of $80/bbl at times this week, including a high of $80.60 today before settling $1.31 higher to $80.06 to close out the week. Tight gasoline supplies and although a bit softer as of late, refinery run rates have posted well above the 5yr averages. Cushing storage continues to drop, falling by 2.6mm bbls per the EIA’s most recent Weekly Petroleum Report. Analysts remain bullish that demand will prove to outstrip supply by the end of August. There are plenty of naysayers as well, with thoughts that futures are overbought and a correction is coming soon.

Link to full report here: U.S. Weekly Petroleum Report

Rig Count

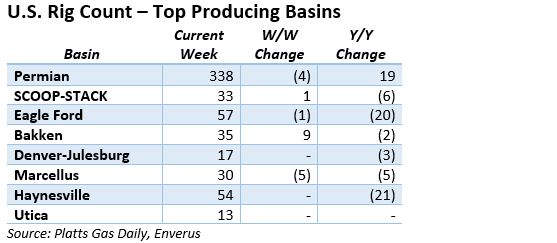

The U.S. oil and gas rig count reversed the previous week’s six rig drop, adding nine on the week to 742. The Bakken accounted for the largest gain of the major basins, adding nine on its own which was offset with the Permian and Marcellus which combined for a nine rig drop. Non-core basins added a net gain on nine as well. Many analysts suspect the overall count is approaching a floor. Investment bank Tudor Pickering Holt recently commented that they still expect another 10-15 rigs to be let go through the balance of 2023. The current total of 742 is well below year-ago numbers, where the rig count sat at 827 for the same week in 2022.

Natural Gas

Natural Gas futures began the week trading steadily in the $2.70 range, but as the longer-term forecast looks to bring some heat relief, futures have felt the impact. Record breaking temperatures have covered much of the US and power demand has been near record levels this past weekend. Floating LNG storage has continued to see gains this week as well as European storage levels. Natural gas storage levels are sitting 13% above the 5-year average, according to this morning’s released EIA report. While these levels may keep a cap on prices, weather remains in the driver’s seat as hotter weather and an active hurricane season will attempt to counter an over supplied market. Prices technically remain in the bull camp, we could see a shift as the choppy trade pattern looks to continue.

Midcontinent demand has strengthened and resulted in natural gas spot prices showing a gain. Chicago city-gates spot prices come at $2.45, a $.17 discount to Henry Hub while NGPL is $.23 back and ANR is $.23. In the futures market, Chicago city-gates is a $.27 discount to Henry Hub while ANR OK and NGPL Midcon are $.35 and $.33 back. According to S&P Global Commodity Insights data, total demand in the Midcon looks to surge to 15.31 Bcf/d, an increase of 613 MMcf/d. In Midcon market area, power demand is forecasted to come in at 6.21 Bcf/d while res-comm demand looks to hit 4.74 Bcf/d. Month-to-date production in the Midcon has increased 3% from last year, coming in at 9.82 Bcf/d.

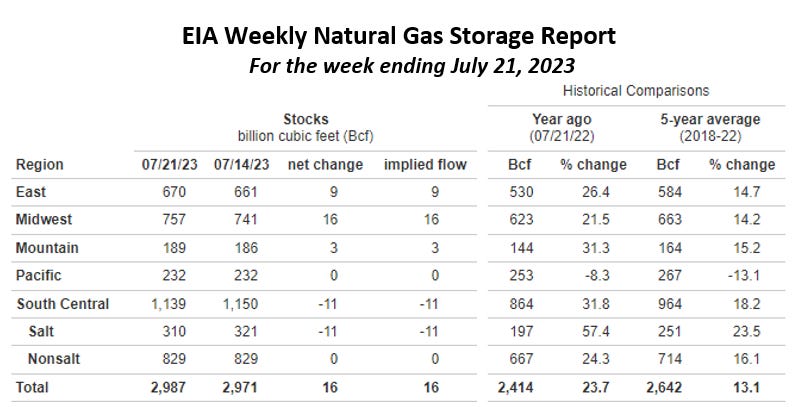

The EIA released storage numbers this morning, coming in at 2,987 Bcf, representing a net +16 Bcf increase from the previous week. This increase was slighlty less than the marketplace expectation range of +21-24 Bcf increase. Stocks were 573 Bcf less this time last year and come in 345 Bcf above the 5 yr. historical range of 2,642 Bcf.

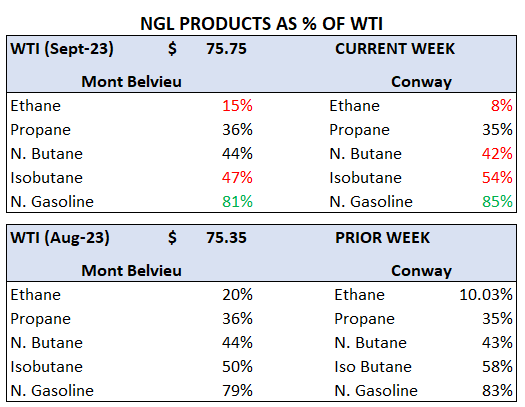

NGLs

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.