Ancova Energy Market Update

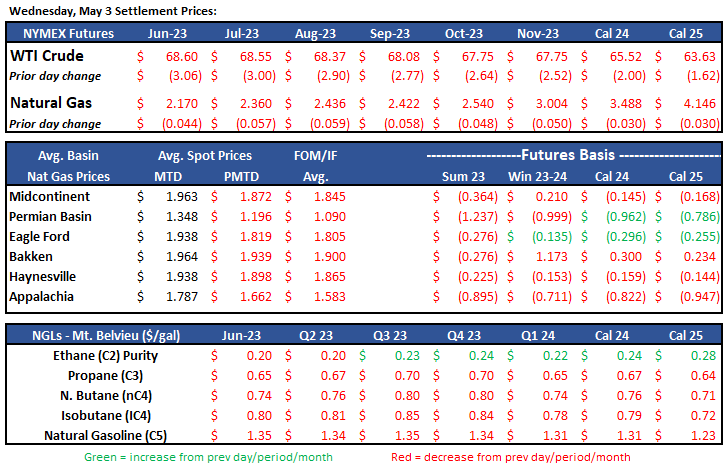

Current Market Pricing

Crude Oil

All bears as of late on the crude front, as prompt-month prices have fallen significantly over the past few weeks. WTI settled comfortably over $80/bbl mid-April, but has been on a downward slide ever since - most recently free-falling as low as $63.57/bbl in overnight trading in what can be described as a “mini-crash”. Prices have since rebounded to near $70/bbl as traders may have oversold their positions. Higher interest rates (including a .25% U.S. hike announced earlier in week), continued challenges within the banking sector, and overall negative consumer spending/traveling sentiment have traders on edge, leading many to believe that a global demand slowdown is inevitable. China’s demand continues to trend upward, but perhaps slower than what the market expected. OPEC+ has decided that its next scheduled meeting in June needs to be in person, a signal that additional action could be taken with regards to production cuts.

The EIA yesterday reported another draw on U.S. crude stocks, this time a slight pull of 1.3mm bbls, moving inventories to 2% below the 5yr average for this time of year. Cushing, America, the physical trading/settlement hub for the NYMEX, went the other way with a half a million bbl increase. On the negative side, total motor gasoline inventory showed a 1.7mm bbl build. Although still 6% below 5yr averages, the build came as a surprise (-1mm bbl expectation) to the market and could be a sign that demand is in fact slipping.

www.eia.gov/petroleum/supply/weekly

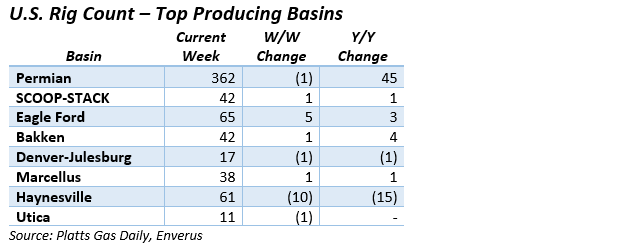

Rig Count Update

U.S. rig count dropped a dozen to 799 on the week to add to its 13-rig decline from previous week. The active rig total is now below 800 for the first time since April 2022. CEOs of Patterson-UTI and Helmerich & Payne both announced in separate earnings calls that they expect to see rig counts fall in Q2 of this year, but expect to see activity pick back up in second half of the year. All moves in the major basins either dropped a rig or added rig, with exception of Eagle Ford (+5) and Haynesville, which had a double-digit fallout on its own.

Natural Gas

Natural gas futures opened the week near $2.40 before experiencing a consecutive 3-day decline. This morning’s trading had prices hovering close to even in an attempt to avoid another finish in the red. Mild weather continues to be the story and has kept late-season heating demand at bay. The forecast looks to remain unchanged for the next two weeks with weather-driven demand likely on the light side. Natural gas production doesn’t appear to be slowing as Haynesville production reached new highs in March, surpassing 2022 daily averages of 13.1 Bcf/d by nearly 10%, according to EIA data. It remains to be seen if producers will react to an oversupplied market, as low prices are the strongest incentive to postpone new activity. As we head into the middle of May, look for the focus to shift to summertime heat driven demand as an attempt to balance the market. Time will tell if it’s enough to flip the market back to the bulls.

With demand taking a tumble in the Midcontinent, spot prices fell across the board. Chicago city-gates fell $.20 to $1.85/MMBtu, while Oneok and NGPL are sitting $.17 and $.26 back respectively. Futures prices have Chicago city-gates $.22 back from Henry Hub, while ANR OK and NGPL Midcon are $.26 and $.33 back. Total demand in the Midcon was projected to drop 1.5 Bcf/d to 14.8 Bcf/d while residential demand looked to tumble to 11.1 Bcf/d according to S&P Global Commodity Insights. Total supply in the Midcon has decreased 2% day over day, representing a 4% decline from month-to-date supply in 2022. Production, however, sits 1% higher than this time last year.

The EIA released storage numbers this morning, coming in at 2,063 Bcf, representing a net +54 Bcf increase from the previous week. This increase was slightly above the marketplace expectations of +53 Bcf increase. Stocks were 507 Bcf less this time last year and come in 341 Bcf above the 5 yr. historical range of 1,722 Bcf.

Natural Gas Liquids

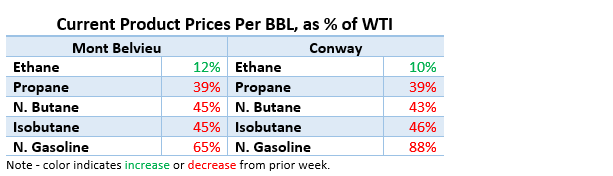

In lockstep with crude prices, products in both Mont Belvieu and Conway took significant price hits. With the new prompt-month contract rolling on, all Propane and heaviers lost anywhere from 13%-43% from same period a week ago. Isobutanes were hit the hardest, losing 43% and 36% of their value WoW. Ethanes were affected the lightest, with MB falling 3% while Conway’s price was the sole gain on the week, adding 13%.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.