Ancova Energy Market Update

Current Market Prices

Crude Oil

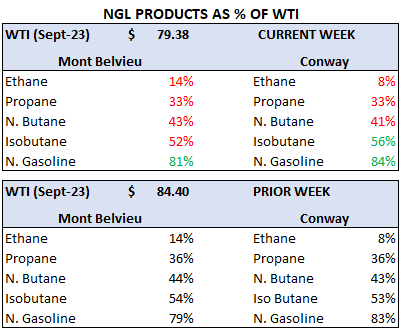

The prompt month WTI contract settled $1.61 lower in yesterday’s trading session to $79.38/bbl and has trended that way since settling at $84.40 on same trading day a week ago. As discussed in last week update, “experts” had warned that the market was in an “overbought” condition and that a corrective phase might be due. A stronger U.S. dollar over the same timeframe along with concerns over China’s fuel demand put pressure on pricing as well. Yesterday’s steep sell-off may have been in lock step with the large stock market drop as the contract has rebounded today, picking up $0.74 to $80.12/bbl at the time this report was written. Some softening of crude prices in the next few weeks is quite possible, as we move from the heavy driving season in September where there’s typically a lighter travel demand. Bullish trends are showing up in U.S. Crude Storage, where the EIA reported yesterday a 4.9mm bbl drop from the previous week making totals 7mm bbls below the 5yr avg.

Full report here: U.S. Weekly Petroleum Report

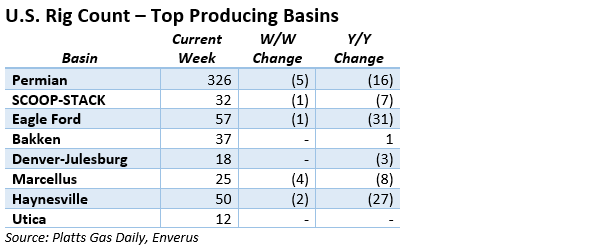

Rig Count

The overall U.S. rig count dropped by nine on the week to 722, making it the lowest # in 17 months. With the five rigs the Permian lost, it is now at an 11-month low and currently sits at 326. The rig count began the year at 866 but has steadily dropped lower, even as commodity prices have recovered/steadied. All major basins dropped rigs or stayed flat on the week and with the overall decline, it’s a common belief that we’re nearing the bottom and should see an uptick over the final few months of the year.

Natural Gas

Natural Gas futures have traded steady for most of the week. After flirting with $3.00 for the majority of last week, trading has made its way back into the mid-$2.60 range this week. Even with hotter temperatures trying to stick around longer than expected, it hasn’t been enough to prevent prices from heading downward. An oversupplied market continues to grab headlines as the US and Europe look well equipped to handle the additional demand being driven by the warmer forecast. Fuel has been added to the fire as rising long-term interest rates have re-kindled a fear in the slowdown of world demand. Look for the bear-bull tug of war to continue, unless a record heat demand push can hop in the driver’s seat throughout September. Traders have been keeping a close eye on multiple Tropical disturbances that could reach the Gulf Coast and create some supply challenges.

As demand has declined in the Midcontinent spot prices followed suit. Chicago city-gates spot prices come in a $.20 discount to Henry Hub at $2.46 while ANR and NGPL are $.26 and $.24 back. In the futures market, Chicago city-gates is trading a $.25 discount to Henry Hub while ANR OK and NGPL Midcon are $.28 and $.31 back. According to S&P Global Commodity Insights data, total demand in the Midcon is expected to fall by 495 MMcf/d, nearing 14 Bcf/d. In the Midcon producing region, power demand looks to drop just under 1.9 Bcf/d with res-comm demand falling to 2 Bcf/d. Month-to-date supply in the Midcon is 9% down compared to the same time last year.

Natural Gas Liquids

All liquid prices in both Mont Belvieu and Conway were down an average of 9% across the board compared to same period last week. Propane in both markets were hit hard, falling 17% and 15%, respectively. Normal Butanes were both down double digits at 10% and 12% and Ethane products in both markets fell significantly as well at 7% and 10%.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.