Ancova Energy Market Update

Current Market Pricing

Crude Oil

The Oct 2023 closed nearly a buck lower yesterday, but remained above $90 at $90.28/bbl in its final trading day as the prompt month contract. U.S. crude storage numbers continue to decline, down 2.1mm bbls which was the same number reported at Cushing, now at a 14-month low and 30% decline since August. Despite a potential supply crunch over the next year, storage is likely to continue its decline given the backwardation in strip pricing. Crude exports also reached a six week high at 5.1mm bpd. The Federal Reserve recently left interest rates unchanged - another bullish factor for crude. The new prompt month contract, Nov 2023, has hovered right around that $90/bbl mark, currently trading $0.38 higher to $90.04/bbl.

Full report here: U.S. Weekly Petroleum Report

Current Rig Count

Total U.S. oil and gas count increased by a single rig to 707, although the core basins picked up a net seven rigs on the week. Oil rigs gained four to 586, with gas rigs dropping three to 121. The SCOOP/STACK in Oklahoma dropped another rig and now sits at 27, down 15 from the same period a year ago. The collective industry minds continue to believe the rig count is at/near the bottom and Q4 2023 and into 2024 should show a steady ramp up given the current commodity strip.

Natural Gas

Natural Gas prices have seen some steady gains this week. Heat returning to the forecast and pipeline maintenance have both aided in the cause. With storage already sitting 6% above the 5-year average and the hottest part of the year behind us, traders are cautious as we head into the fall shoulder building season. The LNG market is a positive as the Freeport facility is back to near full capacity and total US exports are expected to hit 13 Bcf/day this fall. Keep an eye on Atlantic storm activity as any major event could be a price mover, in addition, the Australian worker’s strike remains in the picture and if not settled could add to the volatility. For now, futures look to continue the choppy trend as we greet the fall season this weekend.

Prices in the Midcontinent have been mixed this week as demand has been slow to build heading into the weekend. Chicago city-gates spot prices are a $.53 discount to Henry Hub at $2.24 while ANR and NGPL are $.67 and $.64 back. In the futures market, Chicago city-gates is trading a $.40 discount to Henry Hub while ANR OK and NGPL Midcon are both $.49 back. According to S&P Global Commodity Insights data, total demand in the Midcon is expected to rise to 12.77 bcf/d. In the Midcon producing region, power demand comes in just under 1.5 Bcf/d, while res-comm demand has fallen just under 2 Bcf/d. Month-to-date net flows in the Midcon have dropped under 9 Bcf/d and are 7% lower compared to month-to-date net flows this time last year.

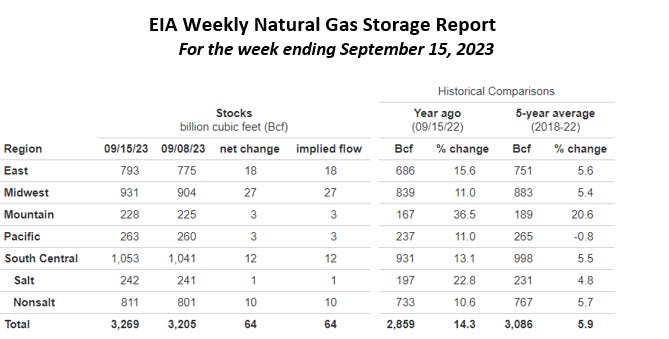

The EIA released storage numbers this morning, coming in at 3,269 Bcf, representing a net +64 Bcf increase from the previous week. This increase was in line with the marketplace expectation range of a +62-70 Bcf increase. Stocks were 410 Bcf less this time last year and come in 183 Bcf above the 5 yr. historical range of 3,086 Bcf.

Natural Gas Liquids

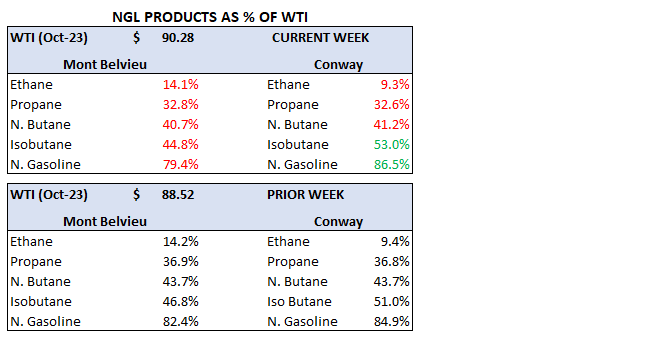

Liquid prices in both Mont Belvieu and Conway markets were mixed compared to same period a week ago, with Propane prices taking a 10% and 11% hit, respectively. Ethane in both markets each had a 1% uptick, with Isobutane in Conway being the biggest gainer at 6%. All other products had minimal movement WoW.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.