Ancova Energy Market Update

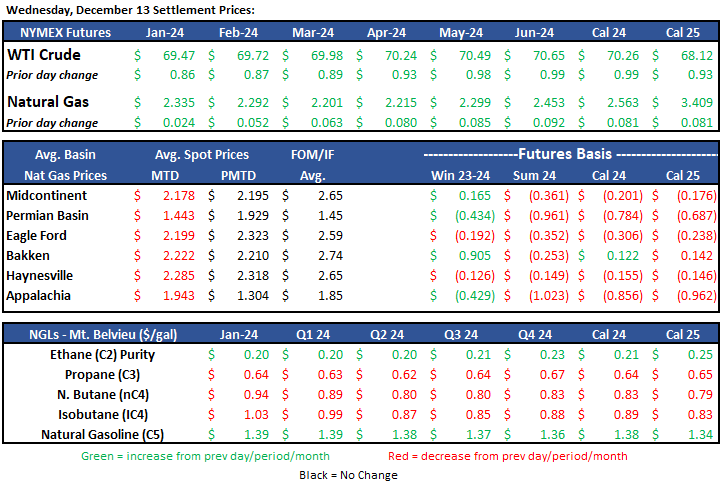

Current Market Prices

Crude Oil

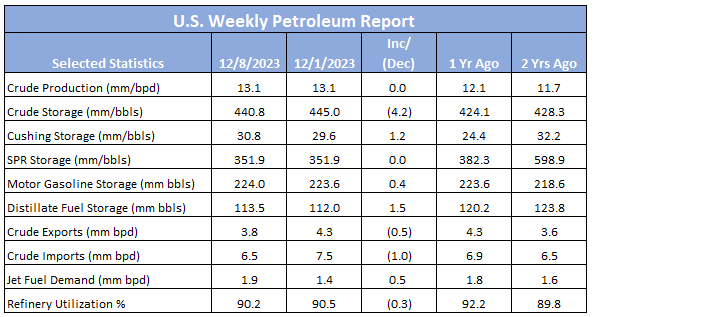

The prompt month contract settled $0.86 higher yesterday to $69.47/bbl, and has surged this morning adding $2.71 to $72.18/bbl. The recent upward momentum likely comes from the Federal Reserve’s statement pointing to lower interest rates which would spark an increase in demand. They concluded meetings on Wednesday leaving interest rates unchanged, but signaling the potential for three cuts across 2024 and have also forecasted a 2% drop in overall inflation (only time will tell). The U.S. dollar also dropped to a four-month low today (weaker dollar = cheaper oil = more demand). U.S. storage posted a larger than expected draw on the week, down 4.2mm bbls to 440.8mm total, but still nearly 17mm bbls higher than a year ago.

Despite the mini-rally, WTI is still ~$20/bbl off from September highs as U.S. production (> 13mm bpd) continues to show strength, butting up against a weakening Chinese economy creating fears that the overall global market is oversupplied.

Full report here: U.S. Weekly Petroleum Report

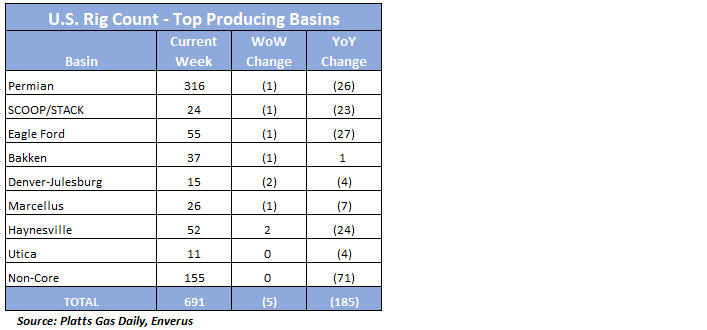

Rig Count

The U.S oil and gas rig count fell by five on the week to 691 keeping below the 700 threshold for the 4th consecutive week. All basins had little volatility on the week, most dropping a single rig with exception of the DJ (-2) and Haynesville (+2). Oil focused rigs settled in a 562 active with gas focused rigs at 129 active. The 691 tally is 185 rigs lowers than last year’s count during same week.

Natural Gas

Natural gas futures hit a 6-month low this week and have continued the downward trend amongst one of the warmest December’s in recent years. A mild weather forecast through the end of December, and low heating demand continue to squelch any thoughts of a wintertime rally. In addition, record production output continues to build on storage levels that are nearly 8% above last year’s levels. Positive notes include analysts predicting prices to climb in coming years with the increased demand of new LNG plants coming into service. US LNG export plants have already hit a record 14.6 Bcfd this month. However, the near term looks to continue the bearish trend as many analysts believe we’ve already seen the peak of winter.

With Midcon demand expected to take a nosedive, regional prices have declined as well. Chicago city-gates spot prices are trading a $.26 discount to Henry Hub at $2.07 while ANR and NGPL are both $.34 back. In the futures market, Chicago city-gates is trading a $.29 premium to Henry Hub while ANR OK is a $.37 premium and NGPL at a $.09 premium. According to S&P Global Commodity Insights data, Midcontinent demand looks to decrease more than 7 Bcf/d to just over 23 Bcf/d. While total production has fallen 2% from the previous day, year to date production in the Scoop-Stack has increased 6% compared to this time last year.

The EIA released storage numbers this morning, coming in at 3,664 Bcf, representing a net -55 Bcf decrease from the previous week. This decrease was slightly above marketplace withdrawal expectations which came in at -52 Bcf. Stocks were 245 Bcf less this time last year, however, this week’s levels are still within the 5 yr. historical range of 3,404 Bcf.

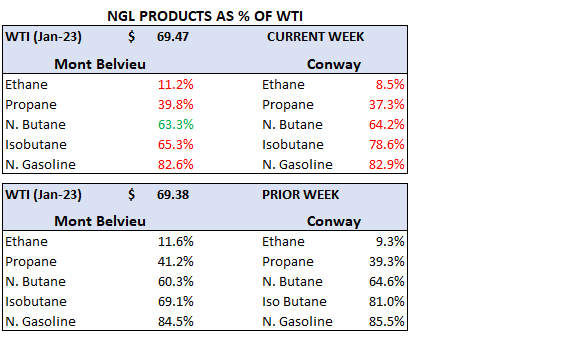

Natural Gas Liquids

Once again product prices in both Mont Belvieu and Conway were lower compared to week ago prices, with the exception of MB N. Butane (+5%). The biggest loser on the week was Conway Ethane, which continues to get hammered (-9%). Purity Ethane in MB took a 3% hit.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.