Ancova Energy Market Update

Current Market Prices

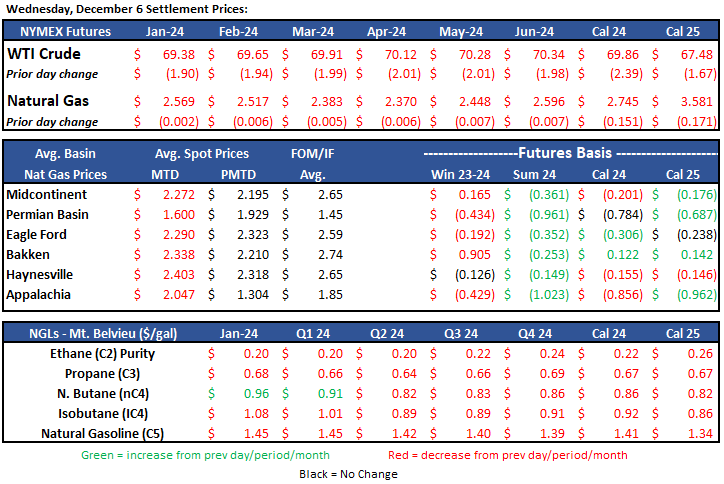

Crude Oil

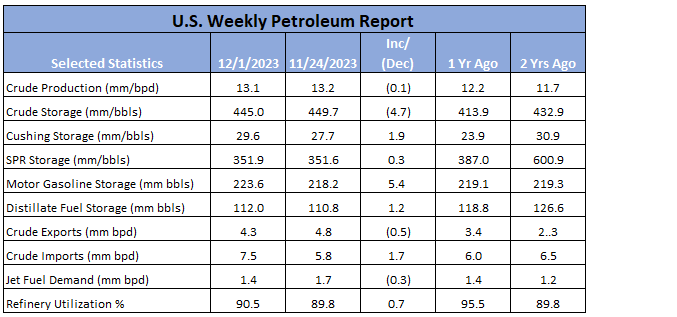

WTI has continued its way lower and lower over the last several weeks, with another milestone yesterday as the prompt month contract closed below $70 to $69.38/bbl. News continues to roll out that global demand is contracting (debatable) and the “voluntary cuts” are not propping up the market like OPEC had hoped. U.S. production also continues to remain elevated and above 13mm bpd. In what is normally bullish news, the EIA released storage numbers yesterday, showing a 4.7mm bbl draw but recent builds have crude inventories closing in on the 5yr avg. Jan 2024 futures contract is further lower again today, currently down $0.53 to $68.85/bbl.

Full report here: U.S. Weekly Petroleum Report

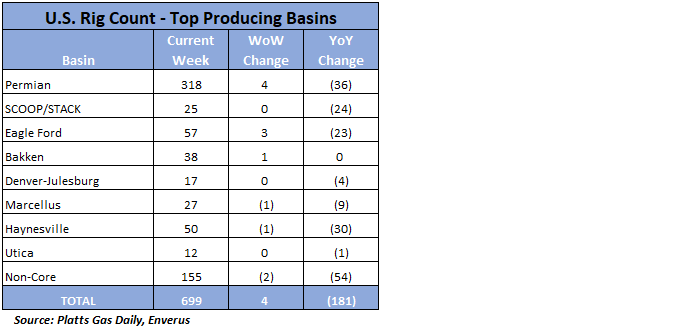

Rig Count

The U.S. oil and gas rig count added four on the week to 699, with a net one add to oil rigs at 564 and a net three add to gas rigs at 135. It was the non-core oil basins that shed majority of the rigs, as the majors (Permian +4, Eagle Ford +3, Bakken +1) combined for a positive 8-rig jump. The combined rig count is now 181 rigs lower than the same period a year ago.

Natural Gas

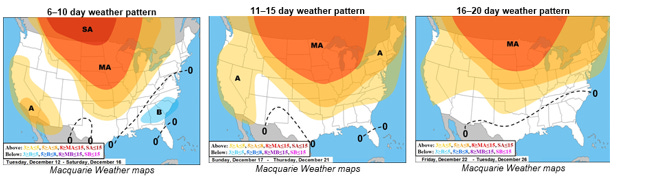

Natural gas futures are feeling the effects of one of the warmest starts to December we’ve seen in recent years. Following a week of steady trading in the $2.70 range, prices have trended downward this week and have held in the $2.50’s in this morning’s trading. Even with long-range forecasts looking to be cooling some, analysts are skeptical of a seasonal January rally. Positive notes include rising LNG imports for China and a triple digit storage withdraw reported in this morning’s report release. While the US & Europe’s storage levels are still sitting at well above average levels, any positive draw bodes well with weather driven demand being non-existence. Look for the market to continue the bearish structure as we anticipate the arrival of old man winter.

The same story holds with the Midcon region as prices have taken a tumble with rising temps and falling demand. Chicago city-gates spot prices are trading a $.37 discount to Henry Hub at $2.36 while ANR and NGPL are $.47 and $.52 back. In the futures market, Chicago city-gates is trading a $.52 premium to Henry Hub while ANR OK is a $.51 premium and NGPL at a $.19 premium. According to S&P Global Commodity Insights data, Midcontinent demand looks to decrease near 4 Bcf/d to 19.29 Bcf/d and the forecast looks to remain above average for the week, quite the contrast to 2 years prior, as temps averaged over 13 degrees below average.

The EIA released storage numbers this morning, coming in at 3,719 Bcf, representing a net -117 Bcf decrease from the previous week. This decrease was slightly above marketplace withdrawal expectations which came in at 99 to 112. Stocks were 254 Bcf less this time last year, however, this week’s levels are still within the 5 yr. historical range of 3,485 Bcf.

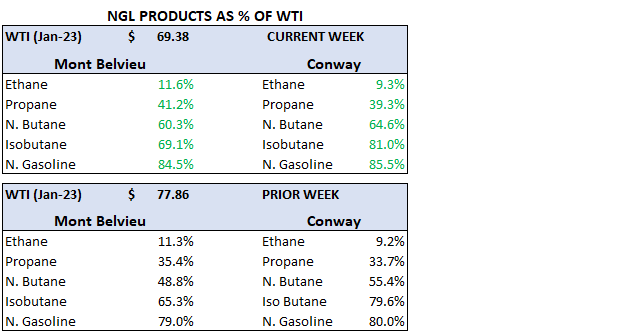

Natural Gas Liquids

Product prices in both Belvieu and Conway were split compared to a week ago with Propane and N. Butane higher (4%, 9% and 4%, 4%, respectively). Ethane prices in both took yet more hits, dropping 9% and 11%, respectively..note that Purity Ethane is now below 20c/gal. N. Gasoline was also down - 5% in each market.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.