Ancova Energy Market Update

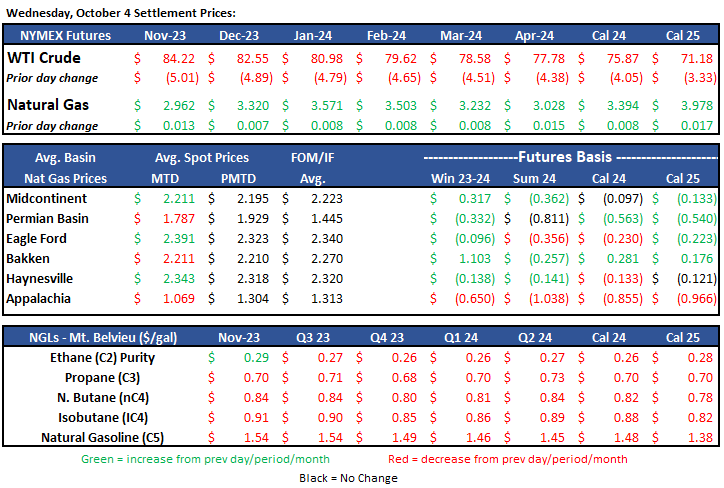

Current Market Pricing

Crude Oil

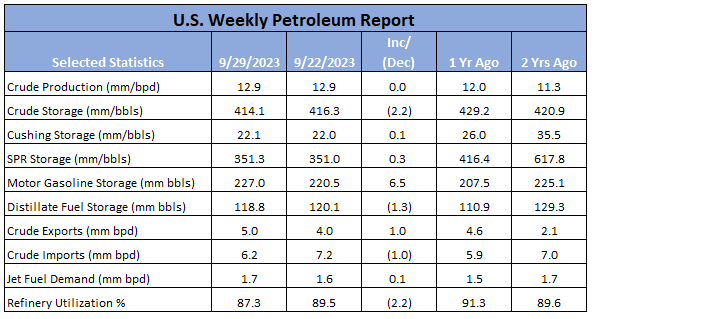

Crude oil has taken a significant hit over the last week, with a majority of the losses coming from yesterday’s session. The prompt month contract dropped just over $5.00 to $84.22/bbl in one of the largest one-day losses this year. The steep drop in the stock market, a large 6mm+ bbl build in gasoline storage (a sign that peak demand is behind us), and U.S. interest rates that are expected to stay high into 2024 were all contributing factors to the free fall. Refinery run rates are also down from previous week, 87.3% vs 89.5% as large refiners begin rolling into maintenance season and taking plants offline. Some have said this correction was inevitable as crude prices had a quick trajectory up into the mid-$90s throughout last month. Crude supplies are still looking to be tight through the winter. U.S. crude inventories are 19mm bbls below the 5yr average (same with Cushing storage levels).

The contract continued its is down again today, trading $1.82 lower to $82.40 as the sell off continues.

Full Report Here: U.S. Weekly Petroleum Report

Rig Activity Update

The U.S. oil and gas rig count dropped another seven on the week to 694, with the Permian accounting for four of those. The Bakken saw a large uptick, adding five rigs to 37 as crude prices continue to ride high. The non-core basins, which are mainly verticals, dropped eight to 156. The SCOOP/STACK in Oklahoma held steady at 26 on the week and still remains at nearly two year lows. Despite higher prices, oil focused rigs dropped 11 to 568, gas rigs increased four to 126. Analysts continue to predict current rig levels are the new floor, and that activity will pick up as we move into the 4th quarter.

Natural Gas

Natural gas futures crossed over the $3.00 mark in yesterday’s session and this morning’s trades have continued the positive vibe as prices have inched up to $3.16. The early week demand pull was triggered by much of the US seeing warmer temps but cooler than expected temps have since moved through the Southeast. With colder nighttime temps predicted for the northern states, next week could spark heating demand as wind chill predictions are calling for the low 40’s, in the meantime, Texas attempts to hang on to their elevated heating demand. While shoulder season typically marks storage re-build and seasonal low prices, thoughts of stronger winter demand and production outages are keeping the hopes alive. November remains with the bears for now but keep an eye on possible upside from export activity and weather triggers to keep things interesting.

With demand rising in the Midcontinent, spot prices have seen an increase. Chicago city-gates spot prices are trading a $.32 discount to Henry Hub at $2.59 while ANR and NGPL are $.47 and $.40 back. In the futures market, Chicago city-gates is trading a $.26 discount to Henry Hub while ANR OK and NGPL Midcon are $.23 and $.38 back. According to S&P Global Commodity Insights data, total demand in the Midcon is projected to rise to 13.76 bcf/d, with power demand accounting for just over 5 Bcf/d. In the Midcon Market region, projections have res-comm demand at 6.7 Bcf/d and power demand at 3.74 Bcf/d. In the Midcon producing area, res-comm demand is expecting just under 2 Bcf/d with power demand near 1.36 Bcf/d

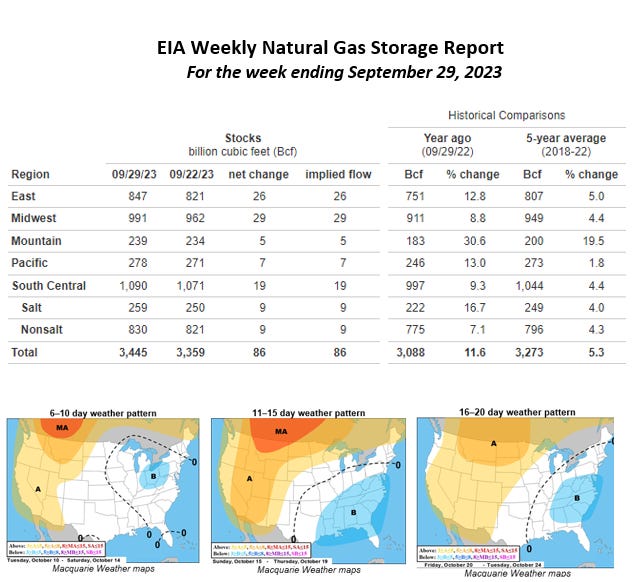

The EIA released storage numbers this morning, coming in at 3,445 Bcf, representing a net +86 Bcf increase from the previous week. This increase was slightly below the marketplace expectation range of +88-95 Bcf increase. Stocks were 357 Bcf less this time last year and come in 172 Bcf above the 5 yr. historical range of 3,273 Bc

Natural Gas Liquids

With the steep drop in crude this week, majority of product prices in both Mont Belvieu and Conway were lower WoW, with exception of Ethane, up 7% in both and Isobutanes, up 1% and 3%, respectively. Biggest losers were Natural gasolines, down 9% and 11%, respectively. All products as a percentage of WTI were higher given the nearly 10% fallout over the week.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.