Ancova Energy Market Update

The Ancova newsletter team will be off next week for the Thanksgiving holiday. The Ancova Energy Market Update will resume the following week. We hope you have a great Thanksgiving with family and friends.

Current Market Prices

Crude Oil

The prompt-month contract continues its downward path, losing $1.60 yesterday to $76.66/bbl. Inventory builds in the U.S. and more specifically Cushing have contributed to further losses, currently down another ~4% or $2.86 to $73.80/bb so far today. This week’s storage build marks the 4th straight week although still well below the five year average (11.8mm bbls) and crude production continues topping the 13mm bpd mark, compared to 12.1mm and 11.4mm bpd 1 and 2 years ago, respectively. Data out of China is showing lower oil processing runs month over month which is reigniting demand concerns, despite OPEC (specifically Saudi Arabia) claiming these concerns are overblown. If today’s losses hold, oil prices will settle at their lowest levels since July.

Full report here: U.S. Weekly Petroleum Report

Rig Count

The U.S oil and gas rig count jumped double digits for the second week in a row, adding 13 to the 15 it gained the week before. Oil based rigs added 18 to 579 while nat gas based rigs fell five to 134, for a combined active total of 713. Despite the solid gains the last few weeks, the overall count is still well below where 2023 began (866). Two large U.S. drillers - Patterson-UTI and Hemerich & Payne are forecasting a 60-70 and 40-60 rig count increase in 2024, respectively.

Natural Gas

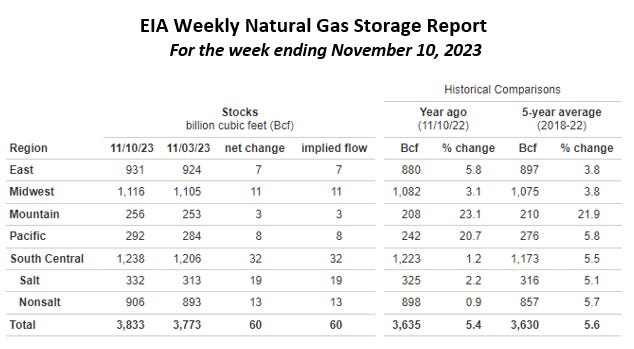

With updated forecasts showing cold weather building the last week of November and into early December, natural gas futures have traded higher this week. After an early week rally fizzled, futures have managed to remain in the $3.20 range for the back half of the week. The anticipated weather-driven demand continues to provide enough spark to keep traders hopeful. While gas inventories in both the United States and Europe look healthy heading into winter, extreme weather and supply interruptions pose risks. Global LNG export and import capacity looks to expand and have more gas available this winter. Export capacity is adding approximately 4 Bcf/d during the winter of 2023/2034, according to EIA’s recently released Global LNG Analysis. With this year’s winter storage levels higher than last season, the market will stay with the bears, while anticipating the winter season demand spike. Prompt month Nat Gas is currently trading ~$0.11 lower to $3.077/MMBtu.

As temperatures increased this week in the Midcon, demand dropped, and prices have seen an uptick. Chicago city-gates spot prices are trading a $.10 discount to Henry Hub at $2.66 while ANR and NGPL are $.24 and $.23 back. In the futures market, Chicago city-gates is trading a $.20 premium to Henry Hub while ANR OK is a $.37 premium and NGPL is $.02 back. According to S&P Global Commodity Insights data, Midwestern demand has seen levels comparable to this past summer. With temperatures ranging from 12 degrees below normal to 12 degrees above, local gas consumption has averaged 2.5 Bcf/d stronger compared to last year.

Natural Gas Liquids

Product prices in both Mont Belvieu and Conway markets have been all over the board this week compared to last week. Propanes were both flat, N. Butanes were both 5% higher, and N. Gasolines both 2% higher despite WTI losses over the course of the week. MB Ethane was down 9% and Conway Ethane was sharply lower with a 33% fallout compared to week ago prices.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.