Ancova Energy Market Update

Current Market Pricing

Crude Oil

The prompt month WTI contract settled $0.79 higher to $72.53/bbl yesterday, and has enjoyed a decent rally from a week ago where it settled near $68/bbl. The 7% rebound was fueled by OPEC stating that they are taking another 1mm bpd off of production (mainly Saudi) and extending all previously stated cuts through the end of 2024. The market expected some action from OPEC but the incremental 1mm was well above most trader expectations. Rig counts continue to drop which will ultimately lead to lower supply, which has likely contributed to the rally. U.S. crude inventory continues to slide per the EIA, another positive boost to prices as the markets expected an increase on the week. The July 2023 contract is giving back a bit of its weekly gains, currently trading $1.59 lower $70.94 as gasoline inventories reported large builds. Traders also appear somewhat nervous about potential rise in U.S. interest rates, which is traditionally bad for crude prices. Expect a Fed pause with no hike this month to be a bullish factor that could send prices considerably higher.

www.eia.gov/petroleum/supply/weekly

U.S. Rig Update

Drilling rig activity in the U.S. dropped a net five on the week - gas rigs fell 10, down to 153 with oil rigs picking up five to 624, for a total of 777 active. The biggest mover on the oil side was in the Bakken, picking up three rigs of the five rigs. Gas rigs continue to tumble as a result of prolonged awful gas prices, which is down from 180 at the start of this year.

Natural Gas

Natural Gas trading has been steady this week. After opening the week at $2.21, prices have flirted near the $2.40 range today. While the early June weather appears to be milder than expected, it has helped keep the floor on prices this week. European prices are increasing with warmer weather on the horizon and LNG prices in Asia could be a trigger for a positive uplift as Russia looks to tighten its supplies. With LNG terminals down due to maintenance issues and exports into Mexico at record highs, eyes are locked on storage as it remains 16% above the five-year average. A heat dome building in the South looks to bring much-anticipated summer heat with temps projected to reach 100 degrees. This will be watched closely as any movement in demand growth could move the needle quickly, until then, the market will stay in a bearish structure.

As demand has inched up in the Midcon, natural gas prices have followed. Chicago city-gates spot prices increased to $.15 back from Henry Hub at $1.96/MMBtu, with Oneok and NGPL come in at $2.00 and $1.95 respectively. In the futures market, Chicago city-gates is $.16 back from Henry Hub while ANR OK and NGPL Midcon are $.22 and $.27 back. Total demand in the Midcon was predicted to reach 13.55 Bcf/d, an increase of 76 MMcf/d with residential-commercial demand expected to top 8.5 Bcf/d, according to S&P Global Commodity Insights data. Production in the Midcon declined to 9.83 Bcf/d with year-to-date production up 10% from last year, while year-to-date supply is 1% higher coming in at 22.12 Bcf/d.

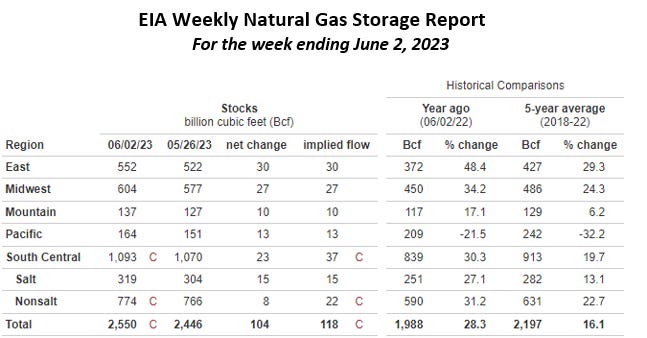

The EIA released storage numbers this morning, coming in at 2,550 Bcf, representing a net +104 Bcf increase from the previous week. This increase was slightly less than marketplace expectations of +117 Bcf increase. Stocks were 562 Bcf less this time last year and come in 353 Bcf above the 5 yr. historical range of 2,197 Bcf.

Natural Gas Liquids

Propane in both markets recovered from the previous week’s crater, rebounding 12% in Mont Belvieu and 8% in Conway. All other products were mixed, with N. Butanes gaining 5% in both markets and Ethane taking losses at 6% and 15%, respectively. All other products stayed relatively constant from week ago prices.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.