Ancova Energy Market Update

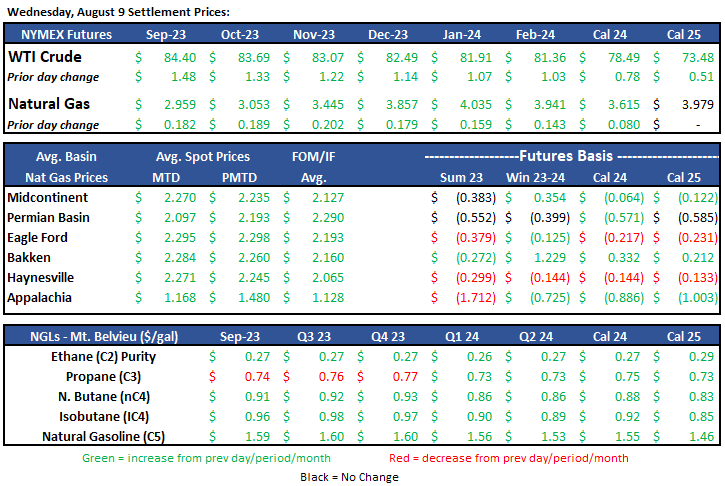

Current Market Pricing

Crude Oil

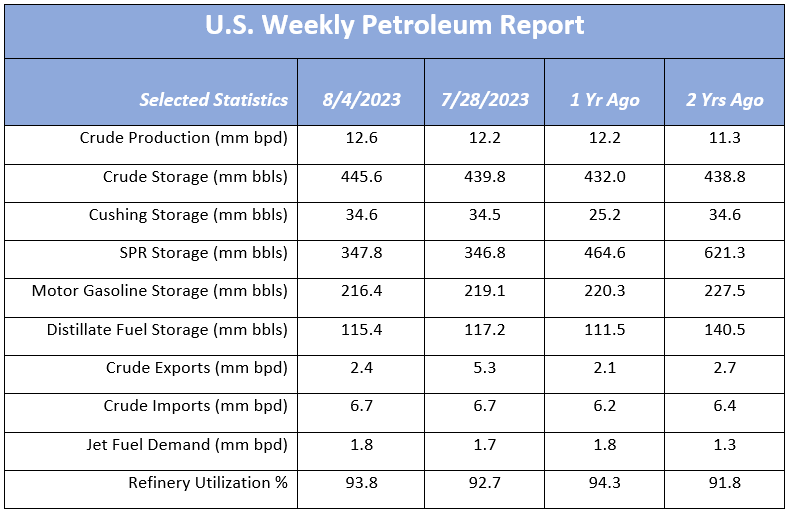

WTI continues showing strength in the face of a presumed upcoming supply crunch, closing $1.48 higher yesterday to $84.40/bbl. Over the last six weeks, the prompt month contract has gained 18.2%. The EIA released what would normally be seen as a bearish report this week, showing a 5.8mm bbl increased in crude storage but sharp drops in gasoline (~9mm) and diesel (~1mm) inventories were the focus. U.S. fuel demand in both of these areas has been unexpectedly strong for this time of year and continues to present concerns for global oil supply. The International Energy Agency is forecasting a 1.7mm bpd oil shortage for the back half of 2023. China remains a wildcard on the demand front as the most recent import figures fell by ~2.4mm bpd to a six-month low of ~10.4mm bpd. It’s not yet clear if this drop is the first of a downward trend as June’s imports were the second highest on record. India’s oil demand is slowing somewhat as well. Both trends have the attention of the Saudi’s which have pledged to extend their 1mm bpd oil cuts through September, and have made comments that extending beyond end of year is not out of the question depending on crude prices.

Despite the summer run-up in WTI, there’s a fairly large group sounding the alarm bells that a global recession is inevitable, which will no doubt have a significant impact on crude prices. Per one trader at BOK Financial “Caution is warranted as futures remain in an overbought condition with a corrective phase due”. Osama Rizvi, contributor to Oilprice.com warns, “I anticipate that bearish sentiment will soon prevail, coupled with profit-taking, ultimately causing oil prices to plummet to the lower $70s or mid $60s. My expectation is that oil prices will reach the lower $60s before the year concludes”. Let’s hope he very wrong.

The Sept 2023 contract has reversed all of yesterday’s gain (and then some), currently down $1.63 to $82.77/bbl.

Link to full report here: Weekly Petroleum Report

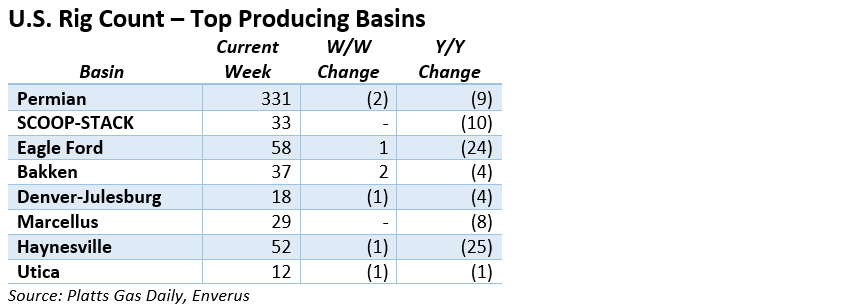

Rig Count Update

The U.S. oil and gas rig count continued its decline through July 2023 despite an increase in overall production volumes (up 6% YoY). Heading into August, the total count was roughly 730 which is down around 143 so far YTD. The Permian has accounted for a significant amount of the overall decrease, and has fallen 33 total since early April alone.

Natural Gas

Natural Gas futures rallied this week after finishing a week that saw futures tumble back to the mid-$2.50 range. In a week that’s seen the longer-term forecast heating back up, trades had surpassed the $3.00-mark by mid-week. While US production remains at high levels, a reduced rig count has speculators eyeing a power demand push that has promise to keep a floor on prices. Record breaking exports are making headlines as EIA indicates US natural gas pipeline exports to Mexico averaged 6.8 Bcf/d during June of this year, which surpassed the previous mark set two years earlier. With US LNG exports expecting to grow substantially in the coming year, it’s worth noting that predictions for a 25% drop in Russia natural gas exports to Europe should be watched closely. As this morning’s storage report comes in with injections above market expectations, September will hold on tight to stay with the bulls.

Midcontinent prices have seen an increase with a slight increase in demand. Chicago city-gates spot prices have seen a nice bump coming in at $2.63, a $.28 discount to Henry Hub while NGPL and ANR come in $.30 and $.31 back. In the futures market, Chicago city-gates is a $.28 discount to Henry Hub while ANR OK and NGPL Midcon are $.30 and $.34 back. According to S&P Global Commodity Insights data, total demand in the Midcon is expected to grow by 112 MMcf/d, nearing 13.88 Bcf/d. In Midcon market area, total demand is forecasted to come in just over 10 Bcf/d with res-comm demand at 5 Bcf/d. Production in the Midcon looks to remain unchanged, however, year to date production is 8% higher than the year prior.

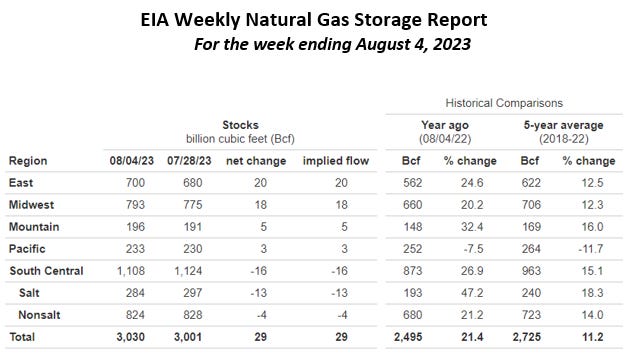

The EIA released storage numbers this morning, coming in at 3,030 Bcf, representing a net +29 Bcf increase from the previous week. This increase was slightly more than the marketplace expectation range of +25 Bcf increase. Stocks were 535 Bcf less this time last year and come in 305 Bcf above the 5 yr. historical range of 2,725 Bcf.

Natural Gas Liquids

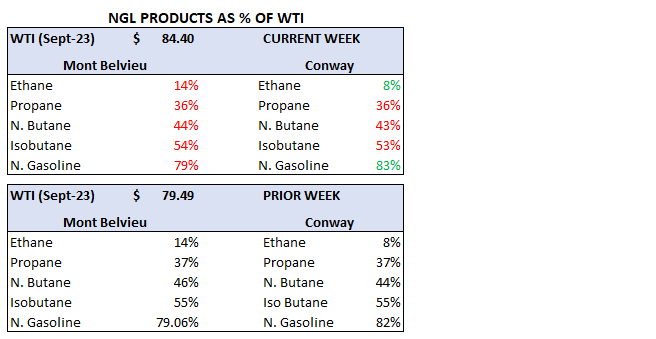

Liquid prices in both markets were all higher WoW, ranging from 1% (MB Propane) to 7% (Conway N. Gas). Compared to % of WTI, majority of products were lower, exception being Conway Ethane and N. Gas, as crude has been on the rise from <$80/bbl to settling at $84.40 last evening.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.