Ancova Energy Market Update

Market Pricing

Crude Oil

WTI has been on a slow decline since our previous report was published - down roughly 8% from last Wednesday’s close price ($74.34). The prompt-month contract closed yesterday’s session down $1.37 to $68.09. It’s believed that OPEC+ will leave production as-is and the Federal Reserve appears to remain vigilant on raising interest rates - two factors that has put pressure on prices and created a selloff the last few days. China’s weaker than expected demand recovery certainly hasn’t help the situation either. Despite a 4.5mm bbl build to U.S. crude storage released by the EIA this morning, crude has shot back up above $70, trading at $70.40/bbl early afternoon and has erased most of this week’s losses. The sharp gain could be a sign that the previous session sell-offs were overdone.

www.eia.gov/petroleum/supply/weekly

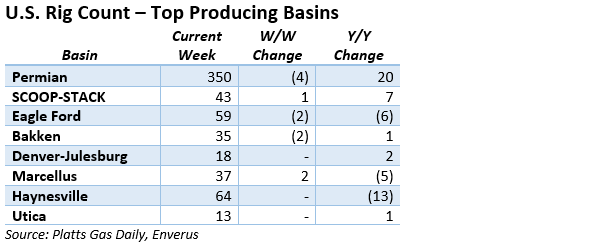

Rig Count Update

The U.S. rig count added a lone rig on the week to 784, and remains at the lowest count since April of last year. The Permian had the largest move, losing four down to 350. The gas focused rigs made an expected drop - down nine to 160 while oil rigs offset the loss by picking up 10 to 624. The count began the year at 866 rigs, but has since dropped 82 with the softening of prices.

Natural Gas

Natural Gas prices have trended downward again this week as the forecasted early summer heat looks less likely. After opening the holiday week at $2.42, prices dipped below $2.20 in this morning’s trading. A few positive notes this week as the US rig count continues the downward trend, floating LNG storage remains down and imported LNG demand has increased in China. The Alberta wildfires continue to make headlines as further production impacts are being monitored. The EPA’s proposed Clean Air Act is also noteworthy, as the new regulations are likely to result in further coal plant retirements, creating more fuel burn opportunities for natural gas. But for now, we wait for the hot summertime heat to bring the anticipated demand pull to price moving levels.

Demand has edged up slightly in the Midcon creating a mixed bag for prices. Chicago city-gates spot prices come in at $1.94/MMBtu, with Oneok and NGPL coming in at $1.77 and $1.84 respectively. In the futures market, Chicago city-gates is $.15 back from Henry Hub while ANR OK and NGPL Midcon are $.35 and $.30 back. Total demand in the Midcon was predicted to reach 13.27 Bcf/d, an increase of 111 MMcf/d with power demand expected to top 5.9 Bcf/d, according to S&P Global Commodity Insights data. Net flows into the Midcon reached nearly 11 Bcf/d to end the month of May as net flows into the Midcon market area reached 14.5 Bcf/d, an increase of 6% to end the month.

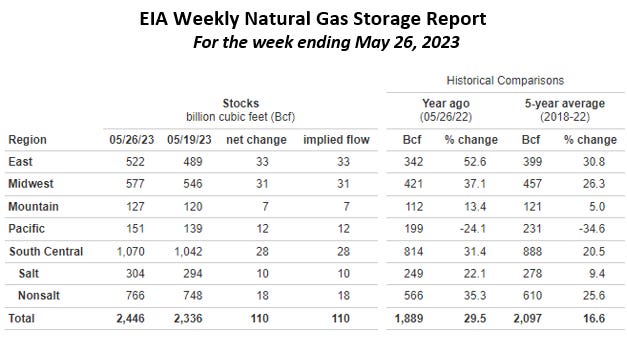

The EIA released storage numbers this morning, coming in at 2,446 Bcf, representing a net +110 Bcf increase from the previous week. This increase was slightly more than marketplace expectations of +103 Bcf increase. Stocks were 557 Bcf less this time last year and come in 349 Bcf above the 5 yr. historical range of 2,097 Bcf.

Natural Gas Liquids

Liquid prices were down across the board week-on-week in both Mont Belvieu and Conway markets given the decline in WTI, which is down roughly 8% from same period last week. MB Propane led the way with a 16% drop followed by Conway Propane at 14%. Normal Butanes were off 13% and 14%, respectively, while MB Natural Gasoline fell 12%. Ethane, which doesn’t typically trend with crude were affected the least, down in both markets 1% and 3%, respectively.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.