Ancova Energy Market Update

Current Market Prices

Crude Oil

WTI futures have continued their downward spiral, opening this week at $80.51/bbl and settling yesterday at $75.33/bbl, with the biggest chunk coming over the last two settlement days’ losses at $3.45 and $2.04/bbl, respectively. Several factors have reportedly played a role here:

Israeli/Hamas war has yet to create any type of supply constraints, as the notion had propped up prices over last few weeks

Weak economic indicators across Asia, with Chinese refineries seeing their lowest margins all year

API data showing a significant build in U.S. storage at +11.9mm bbls, with the Cushing hub at +1.9mm bbl build

Overall weak global demand

While the headlines above are typically in fact bullish for crude prices, several groups, including Saudi Arabia, claims that oil speculators and traders are to blame for the price downturn. “Oil demand is robust - it’s the oil speculators that are behind the most recent drop in global crude oil prices,” said Saudi’s Energy Minister Prince Abdulaziz bin Salman. “It’s not weak. People are pretending it’s weak. It’s all a ploy.” On Wednesday, Saudi Arabia said it would extend its voluntary production cuts of 1mm bpd until at least the end of the year.

The prompt month contract rebounded some early in today’s session, up as much as $1.41 before giving most of it back, currently trading $0.23 higher to $75.55/bbl late in the session.

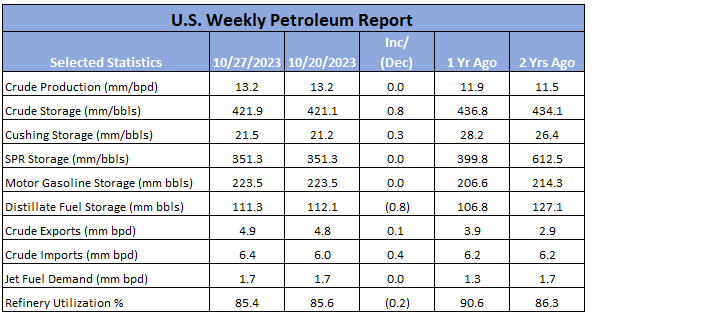

Note: the EIA did NOT release an update this week due to a planned system upgrade and will resume next week.

Full Report here: U.S. Weekly Petroleum Report

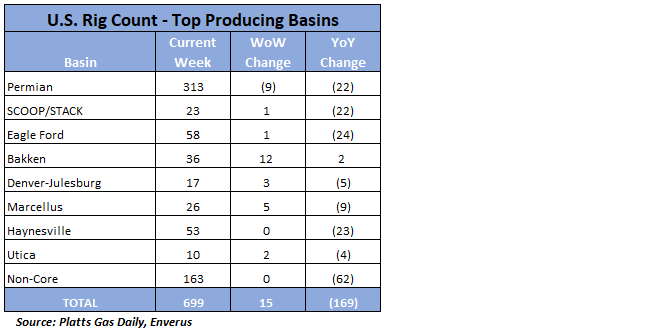

Rig Count Update

U.S. oil and gas rig count rebounded on the week, adding 15 to a notch below 700 at 699 but still remains at the lowest level since late 2021. The full gain came from oil rigs, adding 16 to 569 with gas rigs shedding one to 130. Late 2022 saw 890 rigs but has since shed more than 20% on softer commodity prices and tighter capital budgets.

Natural Gas

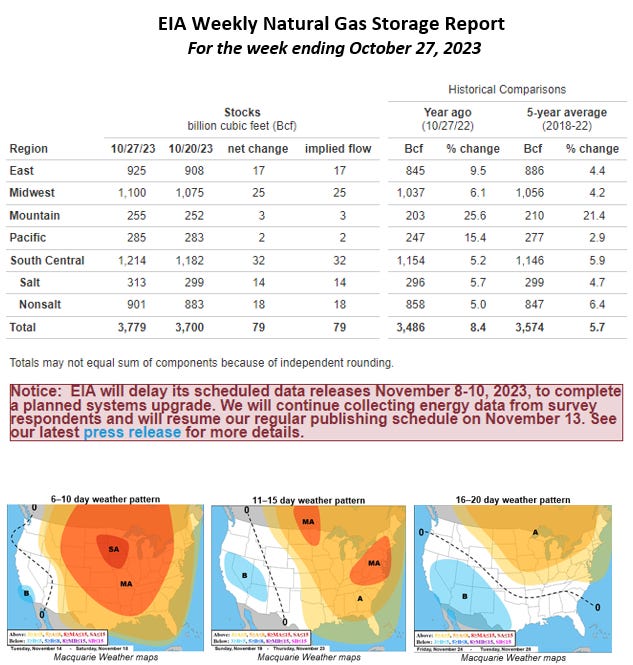

Natural gas futures have been trading lower this week. After an opening of $3.37 to start the week, prices hit a two-week low of $3.02 in this morning’s trading. With milder weather that included spring like temperatures for most of the week, last week’s rally came to a screeching halt. Both US & European storage are running near record levels creating additional pressure for an already over supplied market. With the EIA’s weekly storage report being delayed today, early winter balance assessments will have to wait another week, leaving the market without its key trading catalyst. Heating demand looks to be limited through late November as forecasts are projecting the mild weather to continue, allowing storage injection to continue for at least a few more weeks. The longer-term outlook looks to stay with the bears until we see some freezing temps make their way back into the picture.

With demand strengthening in Midcon, gas prices have seen a boost. Chicago city-gates spot prices are trading a $.02 discount to Henry Hub at $2.19 while ANR and NGPL are $.08 and $.16 back. In the futures market, Chicago city-gates is trading a $.17 premium to Henry Hub while ANR OK is a $.43 premium and NGPL is $.03 back. According to S&P Global Commodity Insights data, total Midcon supply has increased 1% from the previous day but year-to-date supply has decreased by 3% from this time last year. Total Midcon demand looks to rise to just over 17 Bcf/d with res-comm demand up to 13.5 Bcf/d and power demand decreasing to 3.55 bcf/d.

Similar to the U.S Petroleum Report, the EIA is delaying its release of the Weekly Natural Gas Storage Report until next week.

Natural Gas Liquids

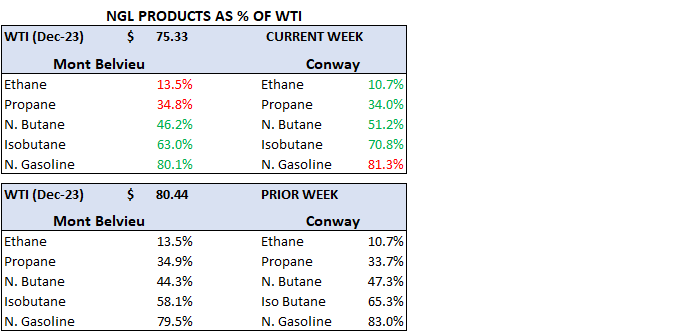

NGL prices in both Mont Belvieu and Conway were predominately lower on the week, with the only gains coming from Isobutanes in both markets, 1% and 2%, respectively and Conway N. Butane at 1%. All remaining products took losses from the previous week ranging from 6%-9%. Biggest loser came from Conway’s N. Gasoline, losing 9% of value in conjunction with WTI.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.