Ancova Energy Market Update

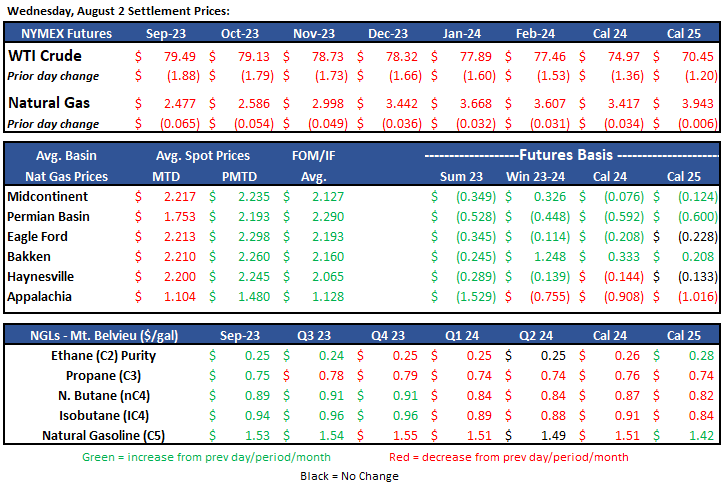

Current Market Pricing

Crude Oil

WTI has seesawed above and below the $80 mark this week but settled $1.88 lower to $79.49/bbl last evening. The U.S. credit downgrade sparked the sharp selloff but was likely kept in check with the EIA’s enormous storage draw - a 17mm bbl decrease from the week prior. With the recent data release, current crude storage levels are now roughly 7mm bbls below the 5yr average. The prompt-month contract has reversed all of yesterday’s loss and then some in today’s trading, currently $2.18 higher to $81.67/bbl as Saudi Arabia announced this morning that it will extend its 1mm bpd production cut longer than expected (~September/October). The oil markets are starting to feel the potential supply crunch which should continue to keep prices moving north.

Full report here: Weekly Petroleum Status Report

Natural Gas

After flirting with $2.70 to start the week, Natural Gas trading has seen a $.20 drop this week as we begin the countdown to the end of summer cooling demand. Brighter notes include Asian demand growth and European storage re-fill. As Europe looks to top-off storage in preparation of wintertime demand, Asia continues to take advantage of the lower prices to fill their demand. Natural gas storage levels are sitting 12% above the 5-year average, according to this morning’s released EIA report and continue to be an upside buffer. Analysts have 2024 LNG exports breaking records which look to provide the much-needed price floor. While production and storage levels remain healthy, look for a major weather event or extended summer heat to provide the shift needed to jump start prices.

Midcontinent prices have dropped despite demand growth. Chicago city-gates spot prices come in at $2.22, a $.21 discount to Henry Hub while NGPL is $.26 back and ANR is $.27. In the futures market, Chicago city-gates is a $.26 discount to Henry Hub while ANR OK and NGPL Midcon are $.27 and $.31 back. According to S&P Global Commodity Insights data, total demand in the Midcon is expected to bump 268 MMcf/d to 14 Bcf/d. In Midcon market area, power demand is forecasted to come in at 10 Bcf/d while res-comm demand looks to fall to 5 Bcf/d. Supply in the Midcon has seen a decrease to 19.76 Bcf/d, a 2% drop from the previous day, while year-to-date supply sits at 21.95 Bcf/d, just above the previous year.

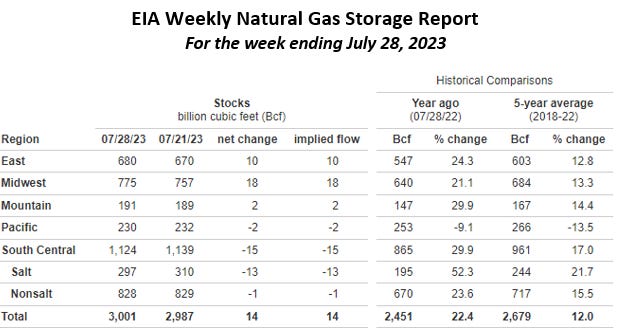

The EIA released storage numbers this morning, coming in at 3,001 Bcf, representing a net +14 Bcf increase from the previous week. This increase was slightly less than the marketplace expectation range of +16-20 Bcf increase. Stocks were 550 Bcf less this time last year and come in 322 Bcf above the 5 yr. historical range of 2,679 Bcf.

Natural Gas Liquids

Prices in both Mont Belvieu and Conway markets are higher across the board with the exception of MB’s purity Ethane, down around 3% compared to prior week. MB Isobutanes were up ~19c or 18% on the week. N. Gasolines were about 2% higher and all others were 7-11% higher.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.