Ancova Energy Market Update

Current Market Pricing

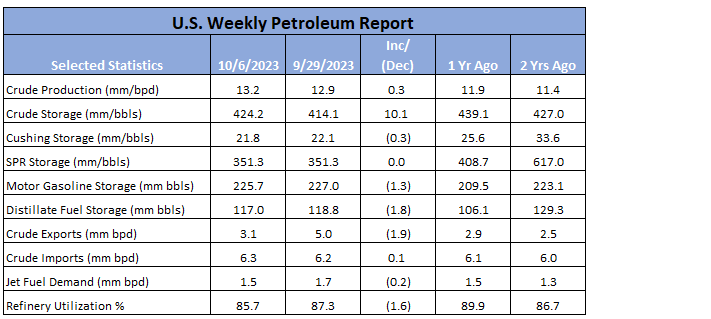

Crude Oil

The prompt month WTI contract has continued to trend down over the last 10+ days, including yesterday with a $2.48/bbl drop to $83.49 on news of a massive 10mm+ bbl increase in U.S. storage. Worries of a global slowdown and impacts from prolonged high-interest rates are primary drivers for the current price reversal. The large build in crude storage can be attributed to the broad refinery maintenance currently happening across the country, and further backed up by the low refinery run rates. Despite the build, global crude supplies remain tight and should support strong crude prices into the winter. Gasoline and distillate storage however showed a drop of 1.3mm and 1.8mm, respectively, as seasonal demand remains on the high side. The Nov 2023 contract has reversed a bit of yesterday’s losses, adding $0.28 to $83.77/bbl.

Full report here: U.S. Weekly Petroleum Report

Rig Count Update

The U.S. oil and gas rig count remained unchanged on the week, with the majority of the basins seeing limited changes, with exception of the Bakken that gave back four of the five that it picked up in the previous week. Oil rigs dropped four to 563 with gas rigs picking up four to 130 to account for the net zero change. There’s still plenty of talk about a modest run-up in over the balance of 2023 and into 2024.

Natural Gas

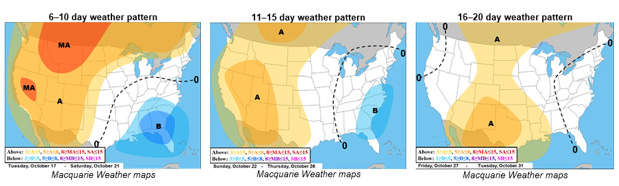

In a week filled with unrest and tensions in the Middle East, the conflict in Israel hasn’t had a huge impact on Natural gas futures, but enough uncertainty exists that Nov contracts have flipped to a bullish structure in this week’s trading. With prices flirting with $3.50 earlier in the week, the $3.30-$3.40 range seems to be the steady mark as we head toward the weekend. Storage numbers are still above the 5 yr average but demand looks to continue its gain as we head into the winter season. The weather forecast looks to be shifting to a cooler pattern for much of the southeast, however, many of the western states are holding tight to their summertime temps. Also worth noting, Australia’s union strike threat is back in the headlines and China remains a buyer in the LNG market as Asian prices are tracking higher. While it appears we’ve seen the seasonal low prices, look for the bumpy ride to continue as prices attempt to keep their grip with the bulls.

With demand falling in the Midcontinent, spot prices have slipped. Chicago city-gates spot prices are trading a $.77 discount to Henry Hub at $2.41 while ANR and NGPL are $.86 and $.85 back. In the futures market, Chicago city-gates is trading a $.34 discount to Henry Hub while ANR OK and NGPL Midcon are $.38 and $.45 back. According to S&P Global Commodity Insights data, total demand in the Midcon is projected to come in just over 14 bcf/d with production in the SCOOP-STACK area coming in just over 1 Bcf/d, an increase of 7% compared to last year.

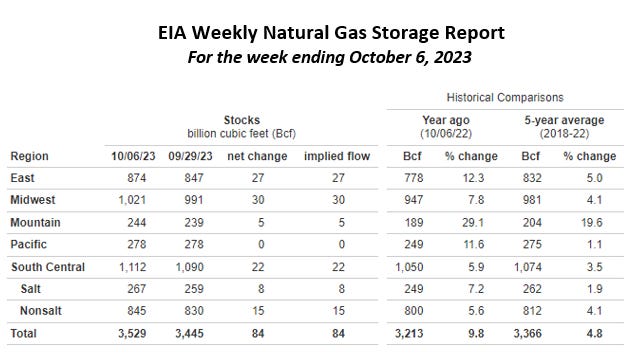

The EIA released storage numbers this morning, coming in at 3,529 Bcf, representing a net +84 Bcf increase from the previous week. This increase was within range of marketplace expectations of +82-90 Bcf increase. Stocks were 316 Bcf less this time last year and come in 163 Bcf above the 5 yr. historical range of 3,366 Bcf.

Natural Gas Liquids

All products across both markets were lower compared to a week ago, with exception of Conway Isobutane (+3%), in line with the continued drop in crude prices. MB Isobutane felt the biggest hit, dropping 8%.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.