Ancova Energy Market Update

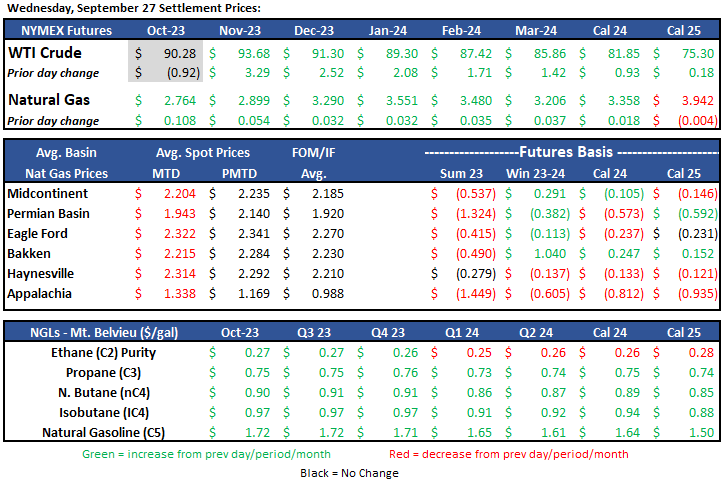

Current Market Pricing

Crude Oil

November 2023 contract shot up $3.29 yesterday to settle at $93.68/bbl as storage continues to shrink at both the Cushing hub and the U.S. as a whole. With Cushing being a significant indicator of future prices, the 900k barrel drop (pushing to 2014 lows) on top of already low stocks continues to drive prices higher. European crude storage is in the same boat showing multi-year lows. Asian fuel demand is also climbing which combined with global storage shortages will continue to keep us in this supply crunch. There’s some chatter that prices have run up a little too much and a little too quickly and the market is overbought, possibly a reason for the selloff in today’s session. The prompt month contract has given back a big chunk of yesterday’s gain, currently down $1.96 to $91.72/bbl.

Full report linked here: U.S. Weekly Petroleum Report

U.S. Rig Count Update

The total oil and gas rig count fell by two on the week to an even 700 active. The SCOOP/STACK combo dropped another two rigs to 25, now at its lowest level in over two years. The Permian dropped three rigs down to 322 and at its lowest count since early Sept of last year. The Bakken also shed three rigs and sits at 32 active.

Natural Gas

After an opening of $2.65 to start the week, natural gas futures are flirting with $3.00 this morning. Gas prices typically trend lower during shoulder season as storage begins to build, however, riding on the coat tails of a crude rally, gas prices are defying the trend. LNG storage is inflated as maintenance has reduced exports and contributed to a 30% increase above last week’s levels. Look for LNG activity to pick up as we head into the winter months. Tropical storms are still making noise, but major hurricanes have managed to dodge the Gulf and have had little impact on prices. With a few weeks of storm season remaining, a major storm may be the only hope for a price rally. US production remains elevated as demand has been subdued with warmer weather in the east and cooler in the west. As October contracts expire today, look for November to continue the volatility and make an attempted run at the bulls.

Both supply and demand have decreased in the Midcontinent, while spot prices have seen an increase. Chicago city-gates spot prices are a $.45 discount to Henry Hub at $2.26 while ANR and NGPL are $.68 and $.67 back. In the futures market, Chicago city-gates is trading a $.33 discount to Henry Hub while ANR OK and NGPL Midcon are $.55 and $.52 back. According to S&P Global Commodity Insights data, total demand in the Midcon comes in at 14.19 bcf/d, with res-comm demand at 8.39 Bcf/d and power demand at 5.12 Bcf/d. Total Midcon supply has dropped to 21.1 Bcf/d, while production has stayed steady at 10.26 Bcf/d.

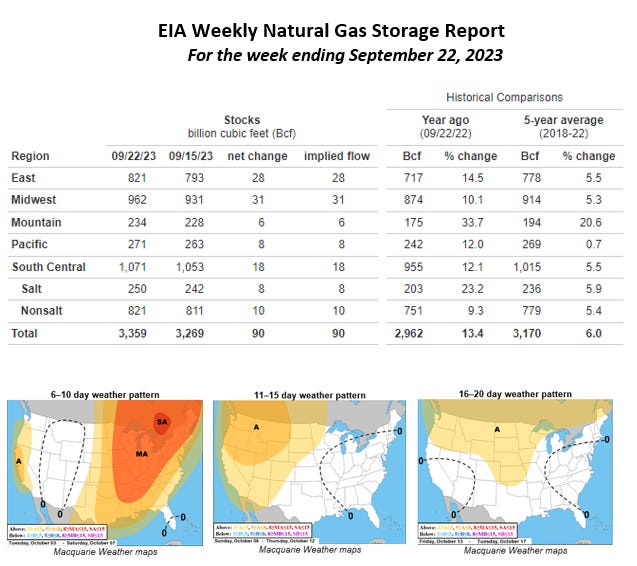

The EIA released storage numbers this morning, coming in at 3,359 Bcf, representing a net +90 Bcf increase from the previous week. This increase was above the marketplace expectation range of a +50-85 Bcf increase. Stocks were 397 Bcf less this time last year and come in 189 Bcf above the 5 yr. historical range of 3,170 Bcf.

Natural Gas Liquids

Product prices in both Mont Belvieu and Conway were mixed compared to week ago prices - purity Ethane in MB taking a 12% hit and Conway Isobutane off 5%. All other products were in the flat to 4% increase range.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.