Ancova Energy Market Update

Current Market Prices

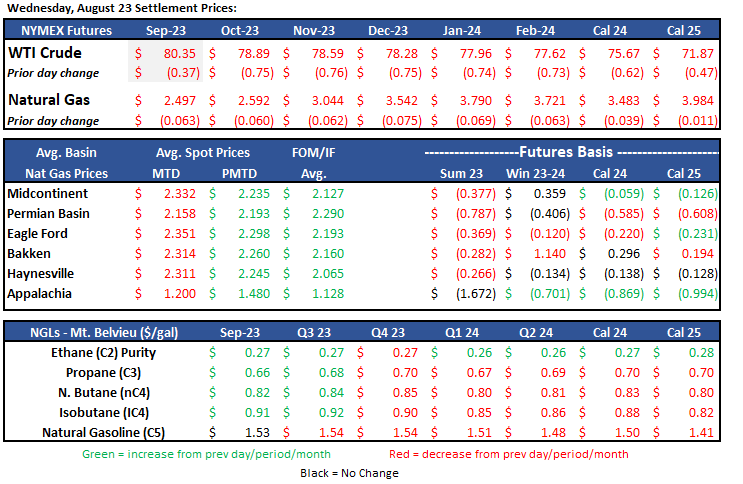

Crude Oil

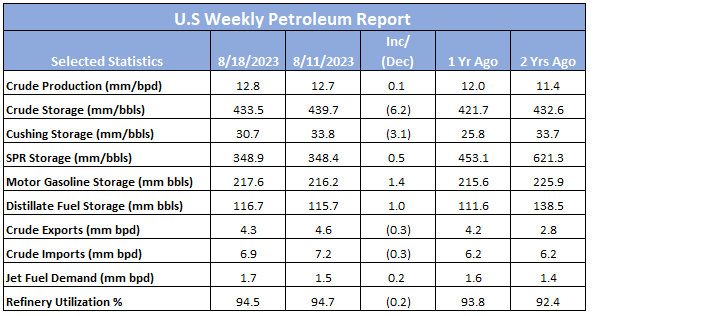

The September 2023 contract rolled off the board Tuesday, settling $0.37 lower to $80.35/bbl. October 2023, the new prompt month contract, has weakened below the $80 threshold over its first few trade days as the U.S. dollar has strengthened and Iranian exports/production has continued to rise - up nearly 3mm bpd which is believed to be at a 4-year high. The potential slowdown of China’s economy also continues to weigh on the market. On the flip side, U.S. crude storage #s were released by the EIA yesterday, showing another large pull at 6.3mm bbls. Cushing also showed a significant drawdown of 3.1mm bbls to 30.7mm and now at 8 month lows.

Full Report Here: U.S. Weekly Petroleum Report

Rig Update

The U.S rig count took another double-digit dip on the week, dropping ten rigs to 712, the lowest count since December 2021. The Bakken accounted for nearly all of the decline, dropping nine on its own down to 28. Between the two commodity groups, gas rigs fell by six, leaving 129 with oil rigs dropping four down to 583. The only core basin to add to their count was the Permian Basin with three, up to 329 and nearly flat to its total from a year ago. Analysts and other industry “experts” are confident that the rig count is nearing the bottom and we can expect some level of “ramp up” early 2024.

Natural Gas

Record temps moved back into the southern states this week and Natural Gas futures rose to $2.66 on Monday. With heat indexes above 100 degrees and OK, TX & LA nearing 110 degrees, cooling power demand has kicked into high gear. Hurricane season has come alive after several weeks of very little activity. Five systems are currently on the radar and look to make some noise in the Atlantic. Natural gas storage, while still 10% above the five-year average, could begin to tighten with extended cooling demand and tropical activity. Also worth a mention are potential strikes at Australia’s LNG plants. While European & Asian inventory levels remain high, threats of a disruption in exports is adding to the price volatility. For now, September outlook stays with the bears as prices remain in the $2.50 range.

As demand has surged in the Midcontinent, spot prices have been at or around $2.60 for most of the week. Chicago city-gates spot prices are a $.25 discount to Henry Hub at $2.34 while ANR and NGPL are $.41 and $.33 back. In the futures market, Chicago city-gates is trading a $.26 discount to Henry Hub while ANR OK and NGPL Midcon are $.28 and $.33 back. According to S&P Global Commodity Insights data, total demand in the Midcon has risen over 2 Bcf/d this week nearing 16 Bcf/d. In the Midcon producing region, power demand has neared 2.7 Bcf/d and res-comm demand comes in just over 2 Bcf/d. While total Midcontinent supply has increased 1% to 20.45 Bcf/d, month-to-date supply is still 10% lower than the same period last year.

The EIA released storage numbers this morning, coming in at 3,083 Bcf, representing a net +18 Bcf increase from the previous week. This increase was less than the marketplace expectation range of +30-35 Bcf increase. Stocks were 513 Bcf less this time last year and come in 268 Bcf above the 5 yr. historical range of 2,815 Bcf.

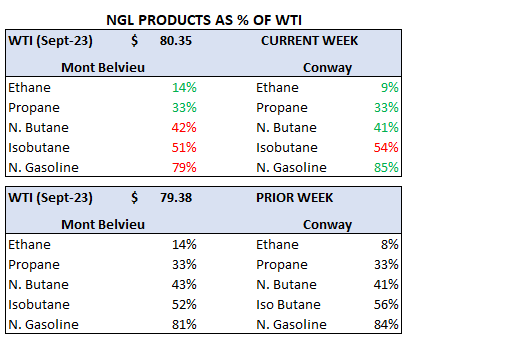

Natural Gas Liquids

Liquid prices in both Mont Belvieu and Conway remained fairly constant from week ago prices, with exception of Conway Ethane which got an 8% bump. Much needed but still sitting low at ~$0.16/gal. All other products stayed within a +/- 3% change.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.