Ancova Energy Market Update

Current Market Prices

Crude Oil

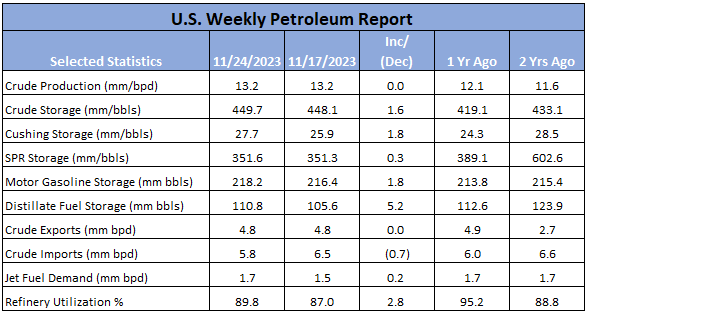

Prompt month crude has continued to hover in the mid-$70/bbl range over the bulk of November, with yesterday being no exception, falling $1.90 to $75.96/bbl. OPEC+ has indicated it will continue to take more barrels off the market in the form of production cuts (2.2mm bpd thru Q1-24), although any cuts from member countries are purely voluntary leaving the market skeptical. U.S. production continues to break new highs at 13.2mm bpd which adds to the overall negative sentiment. The Cal 2024 futures are matching current prices (mid-$70s) indicating elevated production/supply and softer demand throughout the upcoming new year. Prompt month WTI has been fairly flat in today’s session, moving red to green, currently $0.36 higher to $76.32/bbl late morning.

Full report here: U.S. Weekly Petroleum Report

Rig Count Update

The U.S. oil and gas rig count added three on the week to pull back to an even 700 as oil focused rigs dropped five to 572 and gas rigs added a net eight to 128. The Utica was the largest mover with a net three gain, with all others basins at a +/- 2 move on the week.

Natural Gas

After falling to $2.70 early Monday morning following the weekend break, natural gas futures have been holding steady near the $2.80 range for much of the week. Record level production and low weather-driven demand have provided resistance to any potential seasonal price bumps. According to Bloomberg, natural gas production reached 106 Bcf/d in November and is estimated to remain at or near 105 Bcf/d in the near term. With the long-range weather forecast calling for warmer weather across much of the Plains, Midwest and East later this week and into next week, the next cold pattern looks to emerge closer to Christmas. Even with record warm ocean surface temperatures fueling an above-average Hurricane season this year there was little to no lasting impact on natural gas production or prices. It appears the market will stay with the bears in early December as we wait for the wintertime demand to make an appearance.

Midcon prices have decreased this week due to a drop in demand. Chicago city-gates spot prices are trading a $.15 discount to Henry Hub at $2.55 while ANR and NGPL are $.22 and $.24 back. In the futures market, Chicago city-gates is trading a $.62 premium to Henry Hub while ANR OK is a $.74 premium and NGPL is a $.32 premium. According to S&P Global Commodity Insights data, Midcontinent demand looks to plunge near 3 Bcf/d to 22 Bcf/d. Midcontinent supply has dropped 4% day over day coming in at 23 Bcf/d this week, while month to month supply is up 4% compared to last year and year to date supply is 3% lower than previous year.

The EIA released storage numbers this morning, coming in at 3,836 Bcf, representing a net +10 Bcf increase from the previous week. This increase was above marketplace expectations which anticipated -8 decrease. Stocks were 341 Bcf less this time last year, however, this week’s levels are still within the 5 yr. historical range of 3,533 Bcf.

Natural Gas Liquids

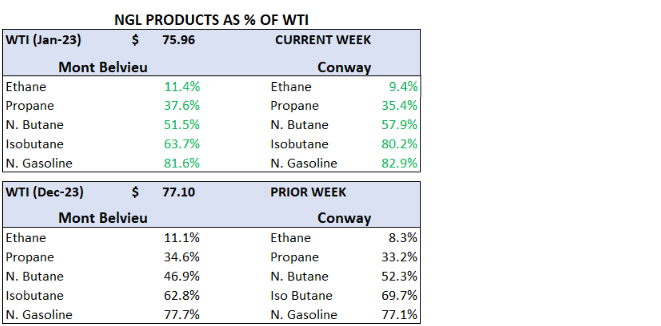

All product prices in both markets were higher from a week ago, with Isobutane and Ethane in Conway jumping 12% and 10%, respectively. N. Butanes were both 8% higher. Purity Ethane in MB showed the the smallest gain, adding 1%. Overall Ethane net prices are for December/January continue to be slim after deducting transportation and fractionation fees.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.