Ancova Energy Market Update

Current Pricing

Crude Oil

Crude prices have continued to move higher over the last week, although down ~1.00/bbl today to $82.29. The rally that began a few weeks ago continue to be propped up with OPEC’s commitment to collectively cut 1.6mm bpd beginning next month, with a good chunk being pledged by Saudi Arabia (500k bpd). China oil demand also continues to provide a bullish sentiment as OPEC announced today it expects the country’s usage to grow by 760,000 to 15.6mm bpd this year compared to last month’s estimate of 710,000 bpd. Overall global oil demand growth is holding steady at 2.3mm bpd as economic uncertainty from monetary tightening by the Fed along with other central banks.

The U.S. energy secretary Jennifer Granholm announced yesterday that the gov’t tentatively plans to begin buying oil to replenish the country’s Strategic Petroleum Reserve (“SPR”) “if it is advantageous to taxpayers”. Purchases would begin in the back half of the year, after the completion of the congressional mandated sales are complete and ending 18+ months of releases designed to stifle oil prices/counter inflation. These statements reverse her comments made to Congress last month so it remains to be seen if and when the potential buyback will occur. Prices on Wednesday saw a 1.6% bump after the news made its way to the markets.

U.S. crude storage showed a slight gain on the week, adding half a million barrels, with Cushing dropping by about the same amount. At 470.5mm bbls, overall storage is approx. 3% above the 5yr average for this time of year. Motor gasoline and distillate fuel inventories on the other hand are 7% and 11% below 5yr averages, respectively.

www.eia.gov/petroleum/supply/weekly

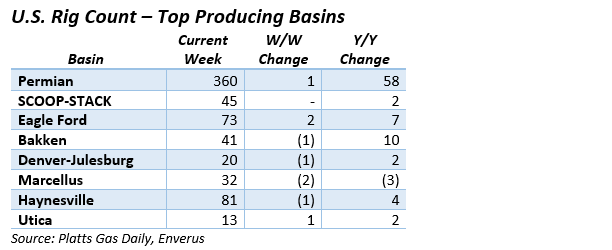

U.S. Rig Count Update

The overall gas total showed a double-digit decline, shedding 13 on the week to 833, 12 of which were gas-focused. With the drops, oil rigs sit at 646 and gas rigs are at 187. Many energy analysts are forecasting another drop of 30+ (some estimates in the 50s) in gas rigs given the current commodity prices, which typically takes some time to make their way through the rigs totals due to ongoing drilling/rig contracts.

Natural Gas

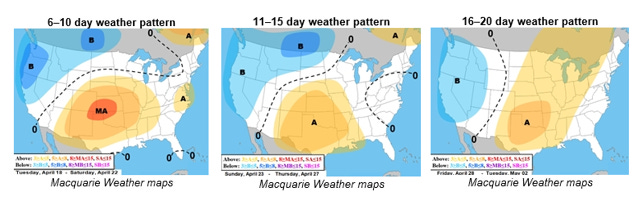

Natural gas futures rallied mid-week after opening just above $2 to start the week. As slightly cooler weather moved across northern parts of the U.S., an increase in national demand contributed to the uptick. The rally was short-lived however, as this morning’s trading saw prices in the $2.02 range. With weather expected to move into a warming trend, demand levels look to ease into typical spring season levels. Europe continues to build storage in preparation for cutting reliance on Russian pipeline gas. Nearly half of Russian LNG exports have been routed to Europe since the start of the Ukraine conflict, which in turn is boosting Russian energy revenues and contributing to war efforts. Even with Europe moving away from Russian dependence, they’ve yet to impose sanctions. On a positive note, analysts are projecting prices to rise above the $3 mark into Q3 with production projected to hold flat and more summertime cooling demand kicking in. Until then look for prices to stay with the bears.

Midcontinent spot prices fell mid-week as Chicago city-gates was down nearly $.15 to $1.85/MMBtu, with Oneok coming in at $1.61 and NGPL at $1.67/MMBtu. Futures prices have Chicago city-gates $.14 back from Henry Hub, while ANR OK and NGPL Midcon are $.21 and $.30 back respectively. Total demand in the Midcon is projected to increase to 11.5 Bcf/d while residential demand is down to 8.2 Bcf . Temperatures in the Midcon market region are forecasted to be about 17 degrees above normal according to S&P Global Commodity Insights.

The EIA released storage numbers this morning, coming in at 1,855 Bcf, representing a net +25 Bcf increase from the previous week. This decrease was slightly less than marketplace expectations of +34 Bcf increase. Stocks were 460 Bcf less this time last year and come in 295 Bcf above the 5 yr. historical range of 1,560 Bcf.

Natural Gas Liquids (“NGLs”)

Prices in both Mont Belvieu and Conway were mixed compared to prices a week ago. Biggest winners were Isobutane (+6%) and N. Butane (+5%) in Conway while the biggest losers were Ethane (-6%) and Conway (-5%), respectively.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.