Ancova Energy Markets Update

Pricing

Crude Oil

At the time of the report WTI is trading at $81.12/bbl. The EIA report that was release earlier today shows production and storage both remaining flat from the prior week.

There is a bill in the U.S. House of Representatives that would prohibit the energy secretary from releasing oil from the SPR without producing oil and gas on federal reserves. President Biden has said he will not sign the bill. After the 221 mm bbl SPR release in 2022, the DOE stated they would refill the SPR for $67-70 per bbl. However, the SPR might not be refilled. The DOE sought to buy 3 mm bbls, and the processes failed. They stated, “DOE will only select bids that meet the required crude specifications and that are at a price that is a good deal for taxpayers.” Many believe they cannot afford to buy at today’s market rate.

With increased demand coming from China, Japan and India, world crude demand hit a 9 month high at 1.7 million bopd. November global demand matched pre Covid demand, while November global production is ~3% below pre Covid.

Last week, Russia’s crude oil exports declined by 22%. Russia is finally feeling the pain of the $60/bbl price cap that the EU implemented in December. However, going forward some expect Russia to drastically increase exports primarily to India. Russia’s energy revenues have fallen and are expected to continue to fall as other countries source crude elsewhere. Russia has responded by placing a five month crude purchase ban on countries that abide by the price cap.

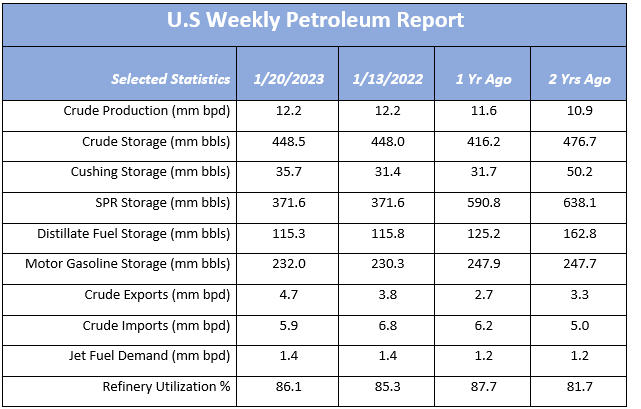

The EIA Petroleum Status Report for the week ending January 20th, 2023 was released earlier today, production stayed the same as the prior week at 12.2mm bbls for the third consecutive week. Crude storage had a small increase from the previous week at 448.5mm bbls. Refinery run rates operated at 86.1%. Jet fuel supplied remained the same as the prior week at 1.4mm bpd.

www.eia.gov/petroleum/supply/weekly

Rig Count Update:

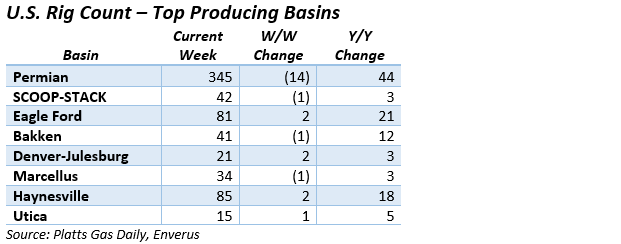

The U.S. O&G rig dropped another ten rigs (855) to continue the losing streak, this off the heals of a 21-rig setback the week before. The Permian accounted for 14 of the net drop, down to 345 but 44 higher than the same period a year ago. All other major basins had limited changes, netting four rigs and bringing down the overall loss to ten. Platts admits that these numbers can be revised as rig count data can lag actual activity, such as rigs moving from location to location, skewing data somewhat.

Natural Gas

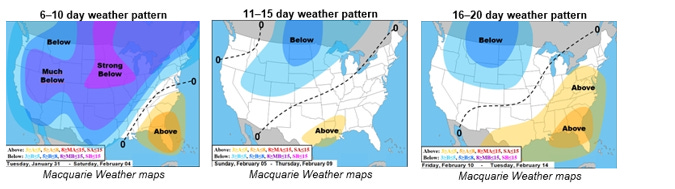

Natural Gas futures opened the week on a rally, increasing by as much as $.30, as it appeared the cold weather moving back into the forecast might do the trick. While prices hit a high of $3.56, the rally would be short-lived as prices had fallen to a nearly two-year low by mid-week and were trading as low as $2.80 this morning. The fears of a wintertime supply shortage have been erased by lack luster winter weather and European inventories continuing to stay at high levels. On the upside, the Freeport LNG terminal has requested permission for a trial restart. Once operational, the boost in US gas exports should provide relief to an oversupplied domestic market and could provide pressure relief on prices. As the wait continues for that wintertime artic boost, look for the bears to continue ruling the market. The 6-10 day forecast is showing a cold snap across much of the country, with Monday and Tuesday of next week showing freezing rain/sleet across a large swatch of the Midcon.

In the Midcon region, total demand looks to increase to 27 Bcf/d by week’s end. The largest increase should come from the residential-commercial sector, according to S&P Global Commodity Insights. Total supply has been held constant at 21.7 Bcf/d as production in the Midcon did increase to 9.3 Bcf/d, however, it was offset by inflows into the region decreasing by 99 MMcf/d. Spot natural gas prices took a tumble this week even with the forecasted demand increase. In the spot market, Chicago city-gates fell nearly $.20 to $2.95. ANR-OK is $.12 back at $2.96 while NGPL-Midcon is $.33 back at $2.75. In forward’s market, Chicago city-gates sits at a $1.35 cent premium to Henry Hub, while ANR-OK is -$.17 back at $2.94 and NGPL-Midcon coming in -$.34 back at $2.77.

The EIA released storage numbers this morning, coming in at 2,729 Bcf, representing a net -91 Bcf decrease from the previous week. This decrease was slightly more than marketplace expectations of – 80 Bcf decrease. Stocks were 107 Bcf less this time last year and come in 128 Bcf above the 5 yr. historical range of 2,601 Bcf.

Natural Gas Liquids (NGLs)

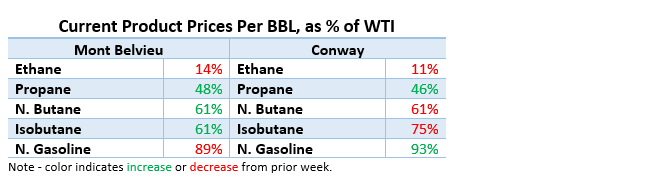

Propane at both Mont Belvieu and Conway saw double digit price increases on the week, 13% and 11%, respectively, on the back of winter weather across the country. Both Natural gasoline prices were 6% higher while the remaining products showed modest change. Conway Ethane got the weekly award for the biggest loser, dropping 4% WoW.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.