Ancova Energy Markets Update

Select Market Prices

Crude Oil

The prompt month contract (June 2023) took a hit in yesterday’s trading, dropping $2.77 (~3.5%) to close the session at $74.30 despite a significant drawdown in U.S oil storage. Apparently concerns of weak refinery profit margins and a potential economic slowdown outweighed the EIA’s report of a ~5mm bbl draw on the week, which is typically a bullish signal and pushes crude prices higher. The market’s sharp turn from $80+/bbl to the mid-$70s is somewhat concerning, considering driving season is just around the corner and crude storage levels are now just below the 5yr average. Motor gasoline and distillate fuels both continue to drop as well - 2.4mm and 0.6mm bbls on the week and currently ~7% and ~12% below the 5yr, respectively. Traders/speculators appear to be concerned with the overall global economy and its affect on demand. Crude is up slightly to $74.64/bbl in early afternoon trading.

In other international news, OPEC Secretary General Haitham Al Ghais commented this morning that the International Energy Agency (IEA) should be “very careful” with its recent comments discouraging investments in the oil industry, citing that such comments would likely lead to oil market volatility. The IEA has been publicly critical of OPEC’s recently announced production cuts of 1.66 bpd, commencing in May and lasting through year-end. Al Ghais reiterated that the cuts were aimed at addressing market fundamentals and not focused on oil prices.

www.eia.gov/petroleum/supply/weekly

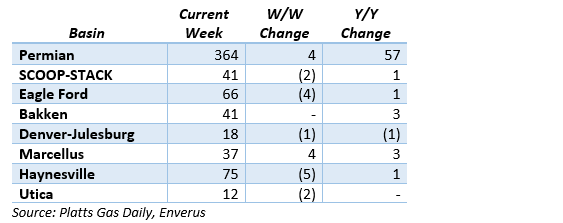

U.S. Rig Count Update

The overall total for the week fell by 13, to 826 led by the Haynesville which dropped five gas rigs to 75. The Permian and Marcellus offset what would have been a bigger drop by adding four rigs each, now sitting at 364 and 37, respectively. Overall, eight of the total 13 were gas rigs, down to 178, with oil focused rigs down five to 648. There’s a widespread expectation that another 30-40 gas rigs will be shed in 2023. Little change in oil rigs counts are expected unless we see significant prices drops throughout the year.

Natural Gas

After opening at $2.22, natural gas futures have made little movement this week. The story continues with production near record levels and an inventory well above the five-year average. With spring weather approaching, the mild outlook looks to keep weather driven demand on the decline. US LNG regained momentum last month as Freeport’s LNG facility ramped up and total shipments set a record of 7.73 million tonnes, according to Reuters. Despite the increases in LNG, there was little to no impact on prices as production continues to increase, and the milder forecasts have heating demand on the decline. With the US natural gas rig count continuing to increase as well, look for the prices to keep the market in a bear structure until producers start reacting to weaker prices.

Midcontinent spot prices felt the impact of falling demand, as Chicago city-gates fell $.15 to $2/MMBtu with Oneok coming in at $2.15 and NGPL at $1.91/MMBtu. Futures prices have Chicago city-gates $.16 back from Henry Hub, while ANR OK and NGPL Midcon are $.20 and $.29 back respectively. Total demand in the Midcon was projected to drop 2.3 Bcf/d to 15.6 Bcf/d while residential demand looked to tumble to 11.8 Bcf according to S&P Global Commodity Insights. Production has increased 1% from the previous day as month to date production is up 10% from the same time last year.

The EIA released storage numbers this morning, coming in at 2,009 Bcf, representing a net +79 Bcf increase from the previous week. This increase was slightly more than marketplace expectations of +76 Bcf increase. Stocks were 525 Bcf less this time last year and come in 365 Bcf above the 5 yr. historical range of 1,644 Bcf.

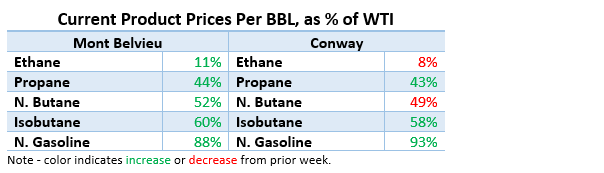

Natural Gas Liquids (NGLs)

All products at both Mont Belvieu and Conway were lower compared to same period a week ago with exception of Isobutane (+4% , 1%) and N. Gasoline (+1%, 3%). Ethane in Conway was hit especially hard, losing 16% while the the remaining products dropped off 4%-6% WoW.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.