Ancova Energy Markets Update

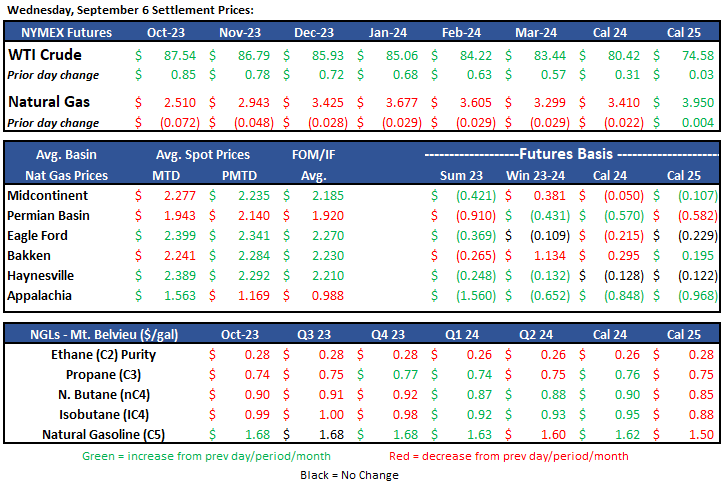

Current Marketing Pricing

Crude Oil

Oil prices have been on a tear across the last several trading sessions. Last week at this time the prompt month contract settled the day at $81.63/bbl and last evening at $87.54/bbl, a tad over 7% increase week on week. Drivers behind the rally are production cuts from Russia and Saudi that have been extended through year-end, which caught crude traders off guard. U.S. oil storage also continues to post significant declines week to week and with rig counts doing the same this sets up for a tight winter supply. The TSA also recently reported that this summer notched an all-time high in travel, showing that demand has remained elevated. On the flip side, China’s economic factors continue to be a cause for concern and futures are in somewhat of an overbought position. These along with any indication of rising inflation could trigger a rapid correction.

October 2023 contracts are trading ~$0.50 lower to $87.08 in early afternoon trading as the U.S. Dollar Index jumped to 105.15, new six month highs.

Full report here: U.S. Weekly Petroleum Report

Rig Count Update

The U.S. rig count dropped another nine rigs on the week to 705, bringing the total to the lowest level since December 2021. Since hitting 889 in November 2022, the overall count has dropped more than 20%. Market analysts and “experts” continue to believe this is the bottom and that rig will be added in Q4 of this year into 2024. Notable year to year changes include the Eagle Ford (-27 or 34%) and Haynesville (-31 or 40%).

Natural Gas

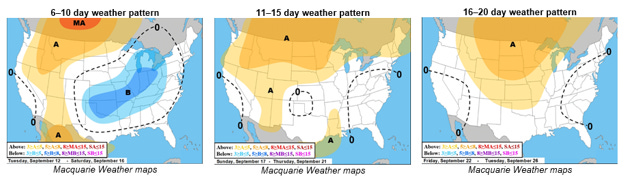

After a week of strong power burn that saw natural gas prices trading higher, prices have trended downward this week as cooler temps are on the way. Last week’s hurricane had little to no impact on production and the hurricane premium appears to be in the rear-view mirror. European storage remains healthy, but an extreme winter could make an impact. The Australian worker’s strike seems to be paused for now but should be watched closely as any disruption in exports adds to price volatility in the LNG world. As we head into supply rebuild season, October prices look to continue the typical lower price trend. Weather and demand stay in the driver’s seat as the longer-range forecast cools off and minimal activity in the Gulf keeps prices with the bears.

With increasing demand in the Midcontinent, spot prices have been mixed. Chicago city-gates spot prices are a $.23 discount to Henry Hub at $2.26 while ANR and NGPL are $.28 and $.26 back. In the futures market, Chicago city-gates is trading a $.31 discount to Henry Hub while ANR OK and NGPL Midcon are $.37 and $.44 back. According to S&P Global Commodity Insights data, total demand in the Midcon comes in at 14.17 Bcf/d this week as power demand fell but residential-commercial demand surged 1.12 Bcf/d to 8.4 Bcf/d. In the Midcon producing region, power demand is just under 1.8 Bcf/d and res-comm demand dropped below 2 Bcf/d. Net flows in the Midcon dropped 6% this week but have increased 5% compared to the same period last year.

The EIA released storage numbers this morning, coming in at 3,148 Bcf, representing a net +33 Bcf increase from the previous week. This increase was less than the marketplace expectation range of +40-45 Bcf increase. Stocks were 462 Bcf less this time last year and come in 222 Bcf above the 5 yr. historical range of 2,926 Bcf.

Natural Gas Liquids

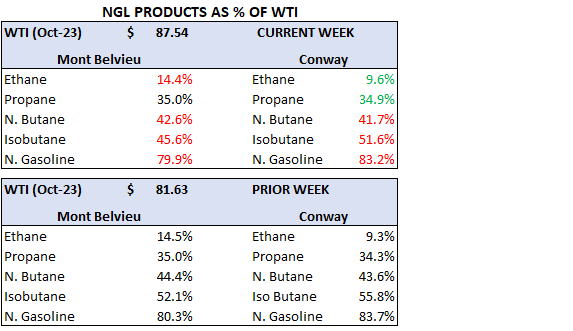

Product prices in both Mont Belvieu and Conway have enjoyed nice run-ups alongside crude, with exception of Isobutanes, down 7% and 1% respectively. Ethane in Conway showed the biggest percentage gain at 10% WoW with the rest of the field picking up between 3-8% compared to a week ago.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.