Ancova Energy Markets Update

Good afternoon, Ancova offices will be closed tomorrow for Good Friday. We hope everyone has a relaxing, long weekend. Thanks for reading, and please reach out with any questions or comments. For the golf fans out there, enjoy the tournament!

Market Pricing

Crude Oil

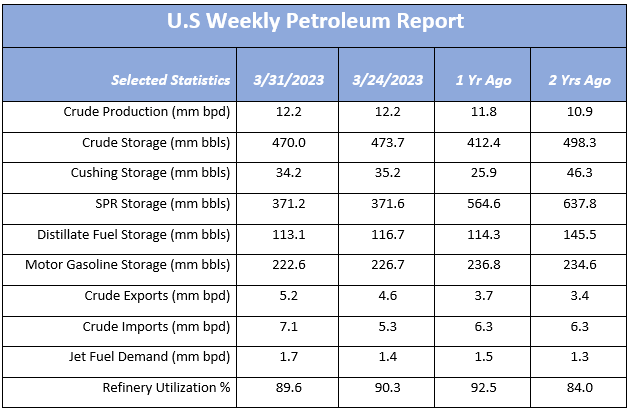

The prompt month crude contract has rebounded sharply this week as OPEC+ threw the markets for a loop, announcing a 1mm+ bpd cut in production effective next month. The announcement last Sunday sparked an ~7% rally in overnight trading, pushing WTI above $80/bbl where it has remained throughout the week. Continued support for the rally has has been in the form of increasing Asian demand + limited Middle East supplies + bullish storage #s released by the EIA yesterday. Crude stocks continue to drop, down another 3.7mm bbls (Cushing accounting for 1mm bbls) as well as Gasoline (down 4.1mm bbls). There continues to be a strong focus on the overall economy as a recession will weigh down demand. CPI and PPI data will be released next week, providing further insight into inflation.

The May 2023 WTI contract is fairly flat on the day, currently trading 11c lower to $80.49. The contract closed a week ago at $72.97 and $69.33 the week prior.

www.eia.gov/petroleum/supply/weekly

U.S Rig Count

Combined rig count added nine on the week to 846, despite the Permian down four. Likely just noise as it pertains to the Permian as the basin has settled in the 350-360 range since mid-November. All other oil heavy basins had small gains with the gas heavy basins netted a one-rig drop. Majority of the gains came from the smaller non-core basins. The rig total is 128 higher than where we sat same period a year ago. According to one investment bank as reported in Platts Gas Daily, expectations are for a 30-50 gas rig drop throughout the balance of 2023 given the plummet in gas prices over the last several months.

Natural Gas

Natural gas futures have managed to stay above $2 this week after seeing a bit of a rally to end last week. With wintry weather moving through the Rockies and Midwest, in addition to strong spring storms in the central US, it was enough to push demand and impact prices. It looks to be short lived, however, with the April forecast leaning towards more moderate weather which won’t call for any increases in heating and cooling demand. According to Reuters, US gas futures have fallen by almost 50% in 2023, after a mild winter that kept heating demand low and allowed utilities to leave gas in storage. Even with some of the biggest players reducing their drilling activity, an uptick in oil prices has kept the drilling incentive in place for others. With US gas production on target to hit record highs this year and gas usage expected to drop, price impacts look to remain minimal and stay with the bears.

Midcontinent spot prices have increased as both demand and supply climbed. Chicago city-gates was up nearly $.05 to $2.05/MMBtu, with Oneok coming in at $1.90 and NGPL at $1.91/MMBtu. Futures prices have Chicago city-gates $.02 back from Henry Hub, while ANR OK and NGPL Midcon are $.11 and $.23 back respectively. Total demand in the Midcon is projected to increase 2.3 Bcf to 18 Bcf/d while residential demand accounts for much of the increase at 2.2 Bcf to 14.4 Bcf total. Supply is up 1% with inflows into the Midcontinent increasing 3% to 11.3 Bcf/d. Month to month supply levels have fallen 4% since this time last year, however, the first three months of 2023 have come in strong and are up 3% from 2022, according to S&P Global Commodity Insights.

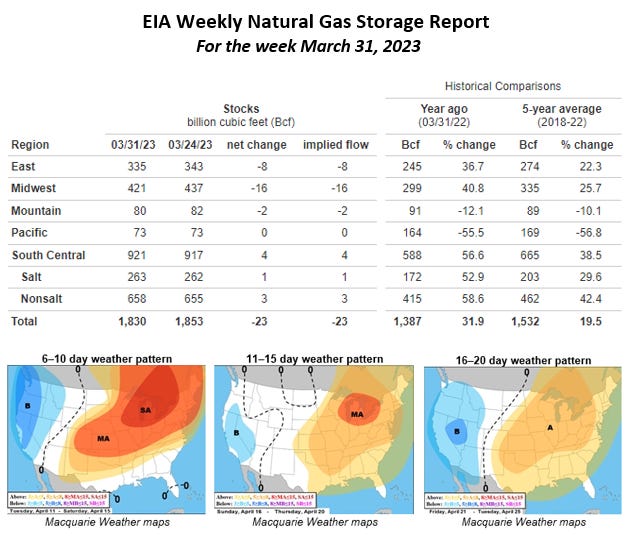

The EIA released storage numbers this morning, coming in at 1,830 Bcf, representing a net -23 Bcf decrease from the previous week. This decrease was slightly less than marketplace expectations of -24 Bcf decrease. Stocks were 443 Bcf less this time last year and come in 298 Bcf above the 5 yr. historical range of 1,532 Bcf.

Natural Gas Liquids (NGLs)

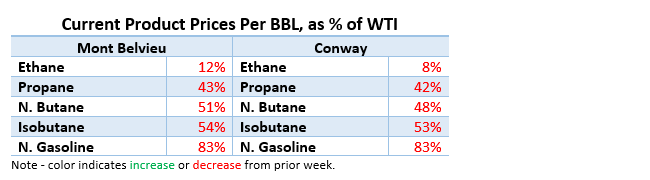

Liquid prices are mostly higher across all products in both Mont Belvieu and Conway markets, with the exception of Conway Ethane (14%) and Isobutane (-6%). Given the strength of crude over the last week, all products naturally took a hit as a % of WTI.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.