Ancova Energy Markets Update

Market Pricing

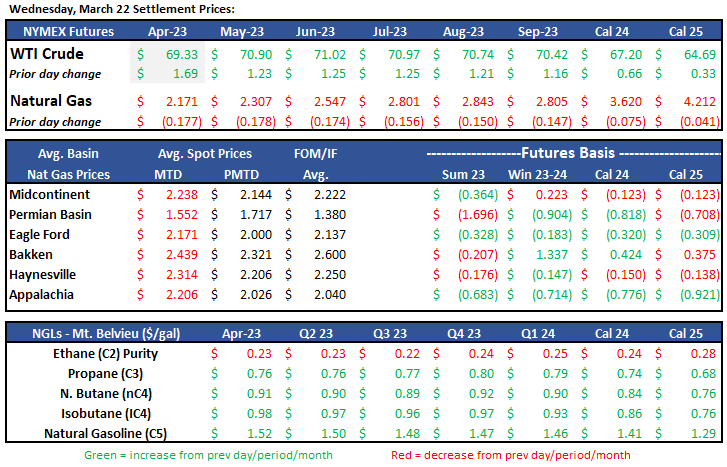

Crude Oil

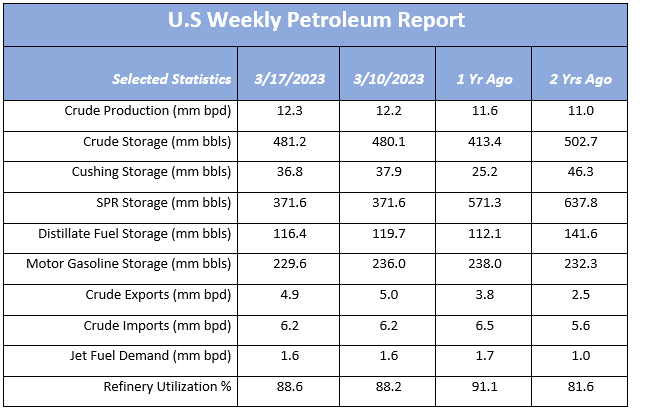

The prompt month NYMEX contract has pulled back to that $70ish range over the last week, but currently trading $1.40 lower today at $69.51. The recent rally has hinged on crude falling off a little too steep, too quickly as China’s demand continues to grow and India’s crude imports have well surpassed last year’s levels. The EIA announced a slight build of 1.1mm bbls to 481.2mm, while Cushing storage dropped the same amount down to 36.8mm. Important to note that overall U.S. crude storage is now 34mm bbls over the 5yr average, its highest level in over two years. The Fed’s decision yesterday to raise interest rates 25 basis points didn’t seem to have much affect on crude prices. The pressure on prices today is likely a result of OPEC+ announcing that it has no near-term plans to make additional production cuts as a result of current pricing.

www.eia.gov/petroleum/supply/weekly

Rig Count Update

The total U.S. oil and gas rig count added four on the week to 843, with both the Permian Basin (362) and the SCOOP+STACK (43) each picking up four rigs as well. Despite the weekly gain rig counts across the country have been in somewhat of a holding pattern so far, which is inconsistent with what operators have indicated for their 2023 plans. Many analysts expect activity to pick up “soon”, although others are citing weaker than expected commodity prices as the main driver for the stand still.

Natural Gas

After opening on an uptick in the $2.25 range this week, Natural Gas futures have dropped to the lower $2 range. With winter trying to hang around into the first part of spring, the forecast looks to be doing its part in pushing for more demand. With storage numbers still holding well above the 5 yr average, the forecasted colder weather appears to be too little too late as we head into the shoulder season. Storage inventories in some European countries have propelled over the 50% capacity mark, with the first injections seen since January. Freeport’s LNG facility suffered operational issues this week and hasn’t given a timeline for ramping back up to full production, further hindering an over supplied market. It looks to be a bumpy ride heading into the shoulder season, with only a major weather or war event able to shift the market away from the bears.

With demand growing in the Midcon region, spot natural gas prices are on the rise. Chicago city-gates increased $.15 to $2.20/MMBtu with Oneok and NGPL up to $2/MMBtu. In the forwards market, April prices fell across the board. Chicago CG comes in $.02 over Henry Hub while ANR OK and NGPL Midcon are -$.16 and -$.29 back respectively. Total demand in the Midcon was up to 18/3 Bcf/d with expectations of additional increases in residential-commercial and power demand in the Midcon market area according to S&P Global Commodity Insights. Net flows into the Midcon are seeing a 9% increase over the previous year, coming in at 8.9 Bcf/d through 3/21.

The EIA released storage numbers this morning, coming in at 1,900 Bcf, representing a net -72 Bcf decrease from the previous week. This decrease was slightly more than marketplace expectations of –70 Bcf decrease. Stocks were 504 Bcf less this time last year and come in 351 Bcf above the 5 yr. historical range of 1,549 Bcf.

Natural Gas Liquids (“NGLs”)

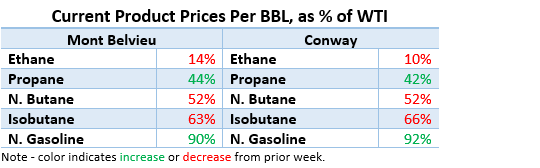

N. Gasoline and Propane in both markets saw 5% and 4% gains, respectively, compared to prices a week ago. Isobutanes took took big hits, losing 11% at Mont Belvieu and 8% at Conway. All other products were either flat or slightly lower on the week.

ANCOVA DISCLAIMER: The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.