Ancova Energy Markets Update

Good morning, and Happy Friday. Sunday will prove to be the day to be outside - triple digits across most of the Midwest today/tomorrow before dropping off significantly the back half of the weekend. Hope everyone has a great one and as always, please reach out with any questions or comments.

Crude Oil

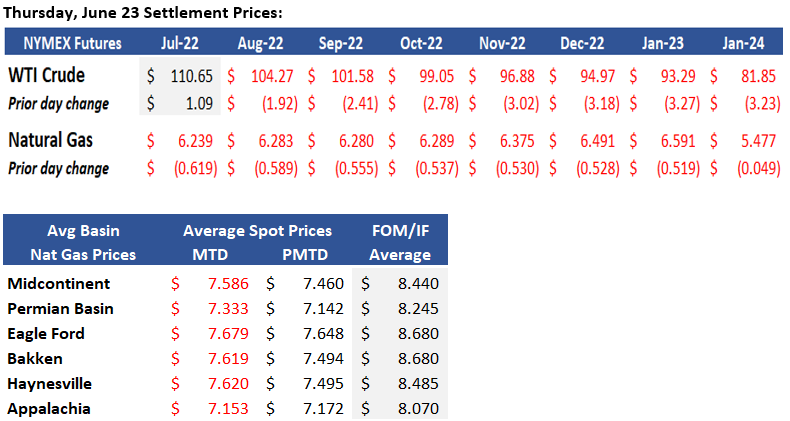

At the time of the newsletter, WTI was trading $3.44 higher to $107.71 /bbl, down ~7% since this time last week. Oil has continued to decrease with concerns of an impending recession which would include a decrease in demand. The EIA reported a large build of crude inventory for the week ending June 17th.

The most recently published Refining Capacity Report by the EIA outlined the decline of refining capacity. Although the US Refiners have been consistently running near max utilization rates, the overall US refining capacity has decreased by 18mm bbls since this time last year. The US has 130 operating refineries today with the capacity to refine just shy of 18mm BBLs per day. Current refinery rates are 16mm BBLs per day. Chevron’s CEO said last week, that it is unlikely that any new refineries will be built in the near future give the current political climate.

President Biden continues to put pressure on the oil and gas industry to lower prices. This week the refineries ran at 94.2% utilization rate the past week. They continue to run at near maximum rates and it is only a matter of time until there is a disruption that causes the run rates to drop.

Iran has drastically increased crude oil exports, doubling from May to June. In May Iran exported 461mm bbls per day and most recent June exports show 961 mm bbls per day. China has and will continue to be the main buyer of Iran crude. Iran is still under sanctions that President Trump put into place in 2018. However, if sanctions are removed and Iran is able to sell globally, some estimate Iran could quickly ramp up to 500mm bbls per day of crude exports.

The U.S. Department of Energy announced last Tuesday plans to sell up to 45mm bbls from the Strategic Petroleum Reserves (SPR). The SPR has fallen to 538mm bbls, the lowest level since 1987.

Per the EIA website, “Several U.S. Energy Information Administration product releases scheduled for the week on June 20, 2022, will be delayed as a result of system issues.” Table below reflects previous week’s data.

www.eia.gov/petroleum/supply/weekly

Rig Count Update:

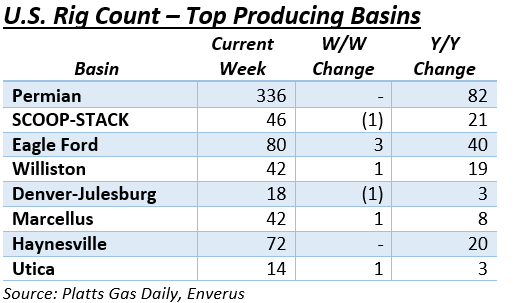

The combined US count was added two on the week to 843, on the heals of the prior week where the count remained unchanged. Oil rigs dropped four to 661, with gas rigs a positive six to 182 through 6/22/2022. The Permian was flat, keeping its rig total at 336 while the SCOOP-STACK lost a single rig for the second consecutive week and now sits at 46 active. Despite the drop in activity, the combined Oklahoma basins are double the count from a year ago. Haynesville also dropped three, down to 72, which is 20 rigs higher than last year. The Eagle Ford saw the most activity, gaining three rigs to 80 in the basin and is now at its highest level since Feb 2020.

Natural Gas

With the market still trying to balance the impacts of Freeport’s LNG terminal outage, Natural Gas futures moved to a 60 day low this week as July contracts landed in the low $6 range. Extreme heat looks to pull heavy cooling demand, but seasonal price tendencies should become less of a price driver as the longest day of the year has come and gone. The uncertainty around Freeport’s prolonged outage has 2 Bcf of gas still being diverted to storage and along with the beginning of hurricane season, the price volatility looks to continue. Looking ahead to winter, if the Russian threat of no gas flow into Europe continues, we are in for another bumpy ride.

The Midcon region has seen mixed prices this week and are hovering the mid-$6 range. ANR-OK is sitting $0.16 back at $6.43 while NGPL-Midcon is $0.25 back at $6.34. Outflows from the Central US rose to 1.62 Bcf/d representing the highest levels in the past week and putting the yearly totals 10% above those seen in June 2021, according to S&P Global commodity Insights. Storage injections in the Midcon Market are following suit as they have averaged a 4.99 Bcf uptick over the last week, while the Midcon Production region reached 870 MMcf/d.

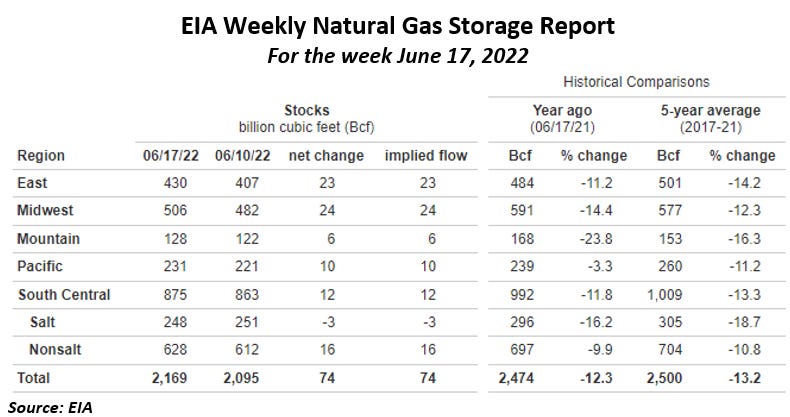

The EIA released storage numbers this morning, coming in at 2,169 Bcf, representing a net +74 Bcf increase from the previous week. This increase was slightly below marketplace expectations +75. Stocks were 305 Bcf higher this time last year, however, this week’s levels are still within the 5 yr. historical range of 2,500 Bcf.

Natural Gas Liquids (NGLs)

N. Gasoline and Ethane across both Mont Belvieu and Conway had significant price drops on the week. N. Gasoline fell 6% and 8%, respectively with Ethane taking deeper hits at 10% and 14%, respectively. Isobutanes moved the other way, gaining 4% and 5%, respectively. Propanes and N. Butanes stayed flat on the week.

Talk Energy Podcast

This week Talk.Energy released episode #127: “Markets, Investing & Avoiding Crypto Scams” with guest Mike Alfred. Mike is on the board of Eagle Brook Advisors and Iris Energy and has decades of investing experience in the public markets as well as experience as an entrepreneur who has built multiple start-ups. Mike was also early on calling out the warning signs on the Celsius Network and Luna Terra collapse. He has been an active voice warning people about the dangers of investing in crypto and Defi projects.

This episode we talk about the current state of the capital markets and how Mike is viewing investing in this environment. We chat about his history as an entrepreneur and the different start-ups he has founded. The discussion moves to Bitcoin mining and Mike’s view on the publicly traded Bitcoin mining companies and where he sees value and risk. Lastly, we discuss the corruption and fraud in the crypto and Defi space and how when things seem too good to be true, they often are.

Episode Video: https://lnkd.in/gnFXkFbD

Episode Audio: https://lnkd.in/gRJ_HqqA

ANCOVA DISCLAIMER: This report may not, in whole or part, be disclosed, reproduced or distributed to others unless you receive prior written consent from Ancova. The opinions expressed in this report are based on information which Ancova believes is reliable; however, Ancova does not represent or warrant its accuracy. These opinions represent the views of Ancova as of the date of this report. These opinions may be subject to change without notice and Ancova will not be responsible for any consequences associated with reliance on any statement or opinion contained in this report. This report should not be considered as an offer or solicitation to buy or sell any securities.